By: Kyle Gardiner

PDF Version: Charter Equality Challenges to the Income Tax Act: The Unsuccessful Streak is Strong, 30 Years On

Research Commented On: Shea Nerland Law LLP Fellowship Project on Tax Law and Equality, Summer 2016

On 2 May, 2016, I began a research project with Jonnette Watson Hamilton, Jennifer Koshan and Saul Templeton examining the role section 15 of the Charter plays in tax law. Over 50 variables were recorded from each of the 134 equality challenges to tax law that we analyzed. To read my post on one of these cases, Grenon v. Canada, 2016 FCA 4 (CanLII), see here. The data promises to be a rich tool for examining equality in the realm of tax law.

When I was conducting a literature review for this project, I reviewed Kathleen Lahey’s “The Impact of the Canadian Charter of Rights and Freedoms on Income Tax Law and Policy” in David Schneiderman & Kate Sutherland, eds, Charting the Consequences: The Impact of Charter Rights on Canadian Law and Politics (Toronto: University of Toronto Press, 1997) 109. In that study, Lahey conducted a review of 300 cases in which Charter challenges were brought to various income tax provisions between 1985 and 1995. The current research extends Lahey’s study, systematically reviewing section 15(1) Charter challenges to tax law that have been brought since the conclusion of her study in October, 1995. While many taxation provisions outside of the Income Tax Act, RSC 1985, c 1 (5th Supp) have seen their share of section 15(1) challenges, the cases examined in our study were specifically section 15(1) equality challenges to a section or sections of the Income Tax Act. Our data awaits further statistical analysis beyond what has been done preliminarily here.

By way of background, section 15 of the Charter is an equality rights guarantee, and it allows claimants who believe they have been discriminated against on the basis of a personal characteristic by a government’s law, policy, or program to challenge that law, policy, or program. Section 15(1) protects against both direct discrimination and adverse effects discrimination. Direct discrimination is usually obvious on the face of the law and occurs where a law’s measures explicitly single out some people for specific treatment because they possess a particular trait. Adverse effects discrimination arises when a neutral rule, applied equally to everyone, has a disproportionate and negative impact on members of a group identified by a prohibited ground of discrimination (see here for a thorough discussion of this distinction). Section 15 reads:

15 (1) Every individual is equal before and under the law and has the right to the equal protection and equal benefit of the law without discrimination and, in particular, without discrimination based on race, national or ethnic origin, colour, religion, sex, age or mental or physical disability.

(2) Subsection (1) does not preclude any law, program or activity that has as its object the amelioration of conditions of disadvantaged individuals or groups including those that are disadvantaged because of race, national or ethnic origin, colour, religion, sex, age or mental or physical disability.

Preliminary Trends

Of the 134 decisions in our study, 114 were challenges heard in the Tax Court of Canada, and 20 were appeals heard by the Federal Court of Appeal. Of those 20 appeals, 13 were appealed from trial decisions that were included in this data set. No challenge succeeded in reaching the Supreme Court of Canada. Leave to appeal was sought in 12 of the 20 Federal Court of Appeal cases reviewed, and was refused by the Supreme Court in each case.

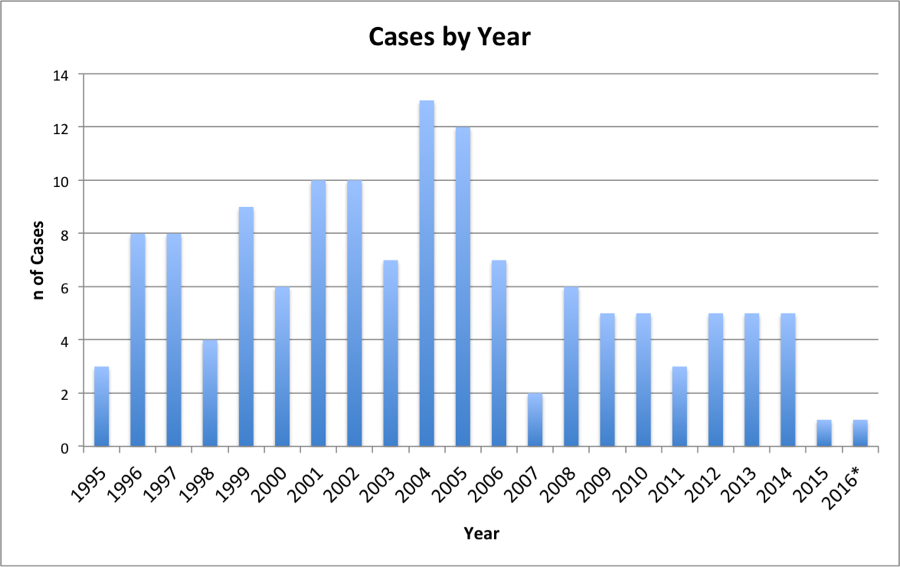

Figure 1 illustrates the chronological distribution of the cases:

Figure 1: Annual distribution of cases reviewed

A wide array of the Income Tax Act’s provisions was challenged in the cases studied. Personal exemptions, exemptions under the Indian Act, RSC 1985, c I-5, deductions for legal fees, childcare expense deductions, moving expense deductions, disability benefits and tax credits, special opportunity grants, various age restrictions, the inclusion/deduction system of child support, the Canada Child Tax Benefit, eligibility for the GST credit, various credits under section 118(5) of the Income Tax Act (including the equivalent to spouse credit and the credit for a wholly dependent person), tuition credits, and tax rates under section 117 of the Income Tax Act were all challenged.

The two most common sections of the Income Tax Act to be challenged were section 118(5) and section 118.2. These sections were followed in popularity by section 56(1)(b), involving the inclusion/deduction of child support payments.

Section 118(5) is a provision that disallows various deductions under section 118(1) to a taxpayer who is obligated to pay support in respect of a child to whom the credit applies. These two sections combine to allow a recipient of child support to claim the relevant credits in subsection (1), while disallowing a payor from claiming the same credits. This provision was challenged 17 times, 15 of which were by male claimants with an obligation to pay child support. The grounds argued here under section 15(1) of the Charter were most commonly family status or sex.

The challenges to this section provide a good example of cases where judges reworked the claimant’s grounds into characteristics that are not protected by the Charter — in these cases, “having an obligation pay child support” or “being a parent who pays child support” (see e.g. Giorno v The Queen, 2005 TCC 175 (CanLII), Calogeracos v The Queen, 2008 TCC 389 (CanLII), and Sears v The Queen, 2009 TCC 22 (CanLII)).

Section 118.2 was also challenged 17 times. These challenges involved the medical expenses credit, 9 of which were specific challenges to section 118.2(2)(n), or the requirement that medications be “recorded by a pharmacist” in order for the claim for a credit to succeed. The section 15(1) Charter grounds most common in these challenges were physical disability, or the type or severity thereof. Female claimants were overrepresented in this category of challenge (9 males to 8 females or 47% females— compared to the 30% of females in the general sample of cases).

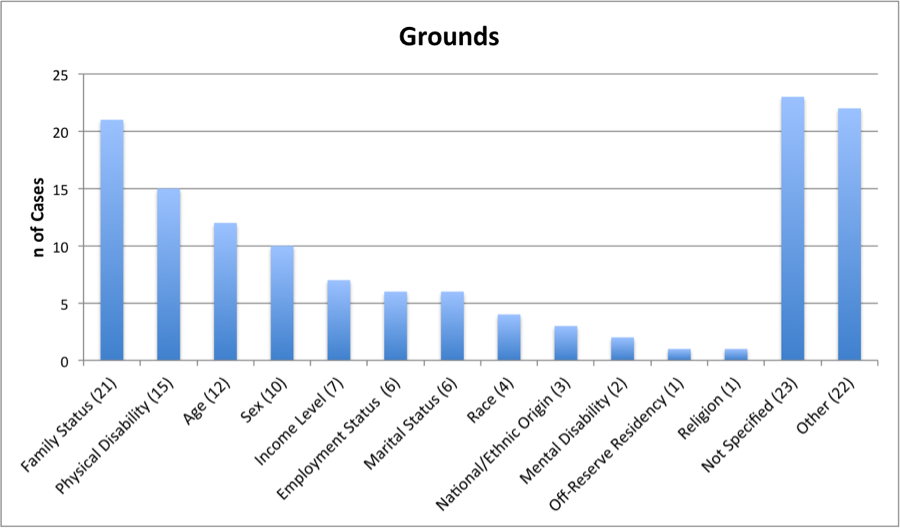

Grounds

Enumerated or analogous grounds refer to those personal characteristics that, if found to be the basis of the discrimination, render the discrimination unconstitutional (if not saved under section 1 of the Charter). Enumerated grounds are those specified in the text of section 15(1), and analogous grounds are those personal characteristics that have been found by the courts to be similarly immutable or constructively immutable (i.e. changeable only at great personal cost). Sexual orientation, marital status, and citizenship are a few examples of analogous grounds.

Of the 134 cases reviewed, 36 contained challenges upon enumerated grounds, 32 upon analogous grounds, and 12 upon both enumerated and analogous grounds. The grounds of the remaining 54 cases consisted mainly of those that were neither enumerated nor found to be analogous to date, or grounds that were not specified. It is important to note that of all challenges reviewed, the “grounds” stage of analysis was the most common point of failure of the section 15(1) claim.

Of the protected grounds, the most common that were argued as the basis for the section 15(1) challenge were family status (21), physical disability (15), age (12), and “other” (22). Common grounds within the “other” category were income sources or level (which we counted separately given our prediction that numerous challenges would be based on this ground), employment status, and inmate status. Fourteen, or 50% of the challenges brought on “other” grounds failed at the grounds stage of section 15(1) analysis. Figure 2 illustrates the grounds argued by claimants in the cases reviewed:

Figure 2: Grounds argued by claimants in the cases reviewed

It is important to note that two of the claimed grounds that appear in Figure 2, income level and employment status, have not been recognized as analogous grounds in Canadian law to date. Because these grounds appeared so often in the cases reviewed, though, they have been given their own categories for display.

Certain claimants brought challenges via multiple grounds under section 15(1) of the Charter. No notable trends appear between the “Grounds” and “Second Grounds” categories, though certain groupings are apparent. For example, age (12) was the most common ground to be coupled with others, namely family status (2), marital status (2), and sex (1). Further analysis of grounds and corresponding second grounds may yet yield useful data or uncover further trends.

Direct Versus Adverse Effects Discrimination

Cases of adverse effects discrimination were more than twice as prevalent as cases of direct discrimination, a divide of roughly 70 to 30 cases. Common issues of adverse effects discrimination were those regarding section 118(5) of the Income Tax Act, where credits could not be claimed for a child because the taxpayer was paying child support in respect of that child, the deductibility of legal expenses (section 60(o)), medical expenses credits (section 118.2(2)), and issues surrounding childcare expenses (section 63). Claims of adverse effects discrimination also appear to be more prevalent among income tax appeals, as only 9 of the 67 section 15(1) discrimination claims heard by the Supreme Court were adverse effects discrimination claims (see Jonnette Watson Hamilton and Jennifer Koshan, “Adverse Impact: The Supreme Court’s Approach to Adverse Effects Discrimination under Section 15 of the Charter” at Appendix 1, as updated to reflect the Supreme Court’s most recent Section 15(1) decision, Kahkewistahaw First Nation v. Taypotat, 2015 SCC 30 (CanLII).

Among adverse effects discrimination cases, the most common grounds argued were family status (14), physical disability (12), “other” (9) and sex (8, 5 males to 3 females). The 12 physical disability cases claiming adverse effects discrimination comprise the entire subset (12) of physical disability cases in our sample. Many of these challenges were to failed claims for medical expense credits under the Income Tax Act.

In direct discrimination cases, “other” grounds were most common (9), followed by age (5) and family status (4). Among the “other” grounds were inmate status (2), sibling status (2), province of residence, cultural rights, and being a receiver of support. The proportion of these grounds within direct discrimination challenges can be compared to the grounds’ prevalence in the greater sample. For example, age represents 17% of all direct discrimination cases, but only 9% of cases in the overall sample were based on the ground of age. As might be expected given that taxation lines are often explicitly drawn on the basis of age, that ground is overrepresented in the direct discrimination category.

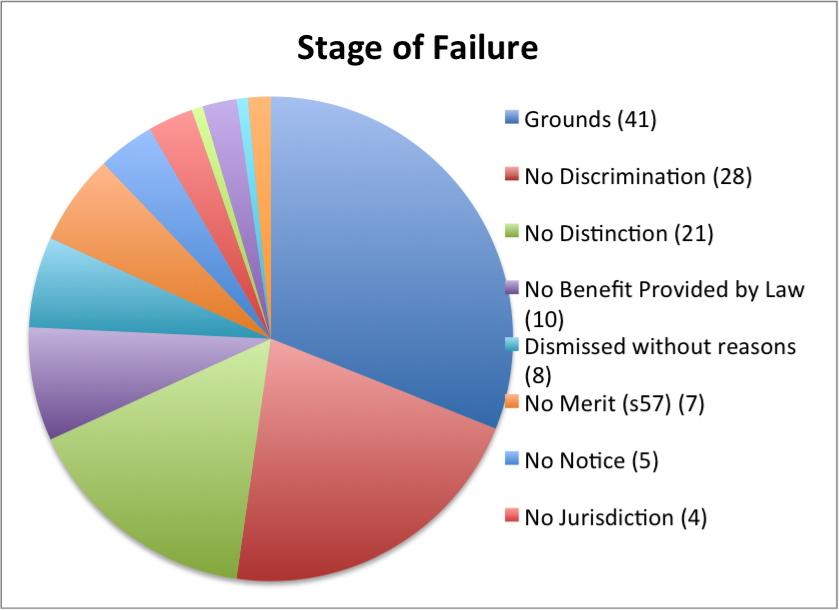

The Failure of all Section 15 Claims

The backbone of the section 15 test requires a claimant to prove a distinction based on an enumerated or analogous ground that results in discrimination. While the framework for section 15 analysis has been in a state of flux since its initial development in Andrews v. Law Society of British Columbia, 1989 1 SCR 143 (CanLII), those core elements have remained.

As noted above, the most common stage of failure in our sample was the “grounds” stage (41), where judges often reasoned that the grounds argued were neither enumerated nor analogous. This result was followed by the “no discrimination” stage (28), and the “no distinction” stage (21). Forty-seven decisions were written by judges who failed the challenge at a second stage, either pointing out multiple stages where the test failed, or proceeding to rule that in the event of an error in the judge’s reasoning, the test would still fail at a later stage.

Anecdotally, “no discrimination” was cited commonly as a “catch-all” reason for failure. See, e.g. Fontaine v. The Queen, 2003 TCC 662 at 10:

The Charter of Rights and Freedoms does not assist the Appellant in any way. He is not discriminated against pursuant to subsection 15(1) or any other section. His Charter argument is frivolous.

Within a 13-paragraph decision in Fontaine, McArthur J.A. disposed of the claimant’s Charter argument in one paragraph. See also Pate v. The Queen, 2004 TCC 190 (CanLII) at 25.

Figure 3 reveals the most common stages of failure of the section 15(1) challenge:

Figure 3: The eight most common stages of failure among cases reviewed.

Among the 134 cases reviewed, only one case was successful at trial, but even this modest success was overturned on appeal (see Wetzel v The Queen, 2004 TCC 767 (CanLII)). In 1984, the federal government and the Conne River Band were negotiating criteria for band membership. In a 1984 order-in-council that included the Band under the Indian Act, the criterion of “Canadian Micmac ancestry” was included, effectively excluding Michael Wetzel— a Micmac of American ancestry— from Band membership and from the tax exemptions that go along with such membership. The Tax Court of Canada ruled that this exclusion was a clear violation of Wetzel’s section 15(1) Charter rights. The remedy granted by the Tax Court was to vacate the tax assessments at issue, a personal remedy under section 24(1) of the Charter. The decision of the Tax Court contains no section 1 analysis of whether the government’s actions were reasonable and justifiable.

This case is anomalous, however. Wetzel involved a remission order, a special remedy under the Financial Administration Act, RSC 1985, c F-11, for waiver of tax when it is unquestionably mandated by tax legislation. Instead of challenging a provision of the ITA, Wetzel’s section 15(1) challenge was brought against an order-in-council. On appeal, the issues were characterized as having more to do with “administrative law wrongs” (see Canada v. Wetzel, 2006 FCA 103 (CanLII) at para 23). Sexton J.A. continued with a section 15(1) Charter analysis, concluding that Wetzel was not treated differently from “all the other residents of Conne River Reserve ‘of Indian Ancestry’”. He concluded on this basis that Wetzel’s section 15(1) Charter rights had not been violated (para 30).

Because the cases reviewed in our study are those containing challenges to provisions of the Income Tax Act, Wetzel does not fit cleanly within our data set. The success that this section 15(1) challenge had at first instance may be attributable to its anomalous nature, but this observation is speculative, and the case was overturned on appeal in any event. That result means that no claimants in our overall sample were successful in their section 15(1) challenges.

Turning briefly to section 15(2), the Charter’s affirmative action provision, it was not determinative in any of the cases reviewed. Because section 15(2) protects ameliorative government laws, policies and programs from section 15(1) challenge, it might have formed another basis for the failure of challenges by taxpayers under section 15(1), but this was not borne out in our sample.

Not only were no cases successful in arguing discrimination under the Charter, no case even succeeded in reaching section 1 analysis— the section of the Charter which allows governments to attempt a justification of Charter violations, if they are found. All of the challenges considered in our sample therefore failed because the section 15(1) arguments were unsuccessful.

Judges

The challenges reviewed in this study were heard at first level by 40 different Tax Court judges. Seven judges heard 49 of the 113 Tax Court of Canada cases. This means that 43% of the cases were decided by just 7 judges. Eighteen cases were heard by 18 different Tax Court of Canada judges who heard only that case during the period under review. That is, there were 18 “one-off” judges.

Claimant Characteristics

Lawyers represented claimants in only 29 cases of the 134 cases reviewed. This is an average representation rate of 22% across both levels of court. Nine claimants were represented by agents, all of whom were law students. One claimant was represented by a relative. The lack of legal counsel across these cases illuminates possible access to justice issues that require deeper exploration.

One other potential access to justice issue is that of cost awards, whereby claimants are either ordered to pay some costs or may have some of their costs of litigation covered (see sections 18.26 and 18.3007 of the Tax Court of Canada Act, RSC 1985, c T-2, under which the court has discretion to award costs). Costs were awarded from the taxpayer in 29 cases, and awarded to the taxpayer in 16 cases. Other arrangements were made in 4 cases, and in the remaining 84 cases cost awards were not specified in the text of the decision.

Claimants were characterized on the face of the decision as “frivolous” 9 times, and “vexatious” 4 times. Frivolous and vexatious claimants never had lawyers and were always male. In the overall sample, claimants were male in 93 cases, and female in 40 cases. In one case the claimant was a corporation. This gender distribution is an exact replication of that found by Lahey in 1997— 70% of the claimants are men. Six claimants were Aboriginal and seeking exemption from payment of taxes under the Indian Act, of which one was Wetzel, the only claimant to succeed in the Tax Court.

While some applications for intervener status were made prior to certain cases being heard, no intervener succeeded in participating in a claimant’s hearing. See e.g. Tall v. The Queen, 2005 TCC 765 (CanLII), where an application for intervener status by the Chinese Canadian National Council (CCNC) was denied in a case involving a section 15(1) challenge based on religion and national or ethnic origin. The claimant in that case sought to claim certain Traditional Chinese Medicine expenses that were not “recorded by a pharmacist” as required by section 118.2(2)(n) of the Income Tax Act. The CCNC intended to offer its unique perspective on issues of equal benefits raised by the claimant’s case.

Finally, 24 cases cited a second Charter section as the basis for the challenge, most commonly section 7 (19 times) and section 6 (5 times). Section 7 protects an individual’s life, liberty and security of the person from government interference that is contrary to the principles of fundamental justice. Section 6 guarantees mobility rights, including the right to move to and take up residence in any province, and to pursue the gaining of a livelihood in any province. Seven cases cited two Charter sections in addition to section 15(1).

Conclusion

The Supreme Court has not heard any section 15(1) challenges in tax cases since the mid-1990s (see Symes v. Canada, [1993] 4 SCR 695 (refusing a claim that the non-deductibility of a woman’s child care expenses as business expenses was discriminatory); Thibaudeau v. Canada, [1995] 2 SCR 627 (refusing a claim that child support payments count as taxable income to the payee was discriminatory)). It was a discouraging surprise to learn that there has not been a single successful section 15(1) claim to the Income Tax Act since then. Nevertheless, the data provides rich opportunities for analysis of section 15 jurisprudence and tax law. I am grateful for the funding received by Shea Nerland Law LLP and for my opportunity to work on this project.

Research for this blog post was made possible by a generous fellowship received from Shea Nerland Law LLP. For more information on the projects funded by this fellowship, see here.

To subscribe to ABlawg by email or RSS feed, please go to https://ablawg.ca

Follow us on Twitter @ABlawg