By: Martin Olszynski, Drew Yewchuk, and Shaun Fluker

Matter Commented On: Alberta’s Mature Asset Strategy: What we Heard and Recommendations Report, April 3, 2025

The Alberta government is poised yet again to change its policy direction for addressing the crisis of unfunded closure liabilities in the conventional oil and gas sector. The current yet-to-be-fully-implemented Liability Management Framework (LMF) was announced – to considerable fanfare – just five years ago, in what seemed like an exchange for $1 billion in federal COVID funding to be applied towards closure work on inactive and orphaned facilities. Now that this federal money has been spent (although $137 million was curiously not spent and had to be returned), and Alberta’s inactive well inventory appears to once again be growing, it is apparently time to abandon the LMF for a ‘new’ policy direction that, if nothing else, will once again delay actually dealing with the problem: enter the Mature Asset Strategy (MAS).

The MAS is the product of a closed-to-the-public selection of working group deliberations chaired by David Yager – an adviser to the premier and an appointed member of the Alberta Energy Regulator (AER) board of directors. This tightly controlled approach to public policy development has become a trademark characteristic of the Smith government, which exhibits strong paternalistic tendencies punctuated with bouts of populism. It is fair to question whether the public would have even seen the MAS before it was implemented, if a draft had not been leaked to the media in March. This disclosure immediately drew concern that the Alberta government was yet again proposing to defeat the polluter pays principle by using public dollars to pay the industry’s closure costs (i.e., the costs of abandonment, increasingly referred to as decommissioning), remediation, and reclamation of inactive oil and gas sites and infrastructure. The official version (dated April 3, 2025) essentially tracks the originally leaked version, with some minor changes around the language of government support.

As a policy roadmap, the MAS is a remarkable document. Some parts are relatively rich in details and specifics, while other parts have almost no details or specifics at all. It contains a few useful (and surprising) admissions and a couple potentially promising ideas, but on the whole it focuses on the wrong problems and ultimately promotes deregulation and thinly disguised new government assistance for the oil and gas industry. It obfuscates the real issues rather than illuminating them. Like the still roughly 80,000 inactive wells that continue to languish on Alberta’s landscapes, then, the MAS should be abandoned post haste, and a formal public hearing process should be set up in its place. As further discussed below, the Alberta Utilities Commission’s (AUC) government-mandated review of closure liability requirements for renewable energy projects provides a good template for what could and should be done relatively quickly.

Our post proceeds as follows. In Part I, we comment on the process leading to the MAS’ development and describe how the problems with the process contributed to the problems with its substance. In Part II, we summarize the analysis and recommendations in the MAS, focusing both on those parts that we find most problematic and those we find useful towards addressing Alberta’s unfunded closure liability crisis. As we explain below, the MAS goes to great lengths to avoid assigning responsibility to government or industry for this crisis. This significantly undermines its credibility because the origins of this crisis have been well-documented, and the primary culprits are government and industry leadership. More specifically, the causes are an exceedingly lax liability management regulatory regime designed and lobbied for by industry leadership at the turn of this century, and a “brisk trade in junk assets” roughly a decade ago. Part III briefly discusses government plans for the implementation of the MAS, while Part IV concludes.

I. The Process for Developing the MAS

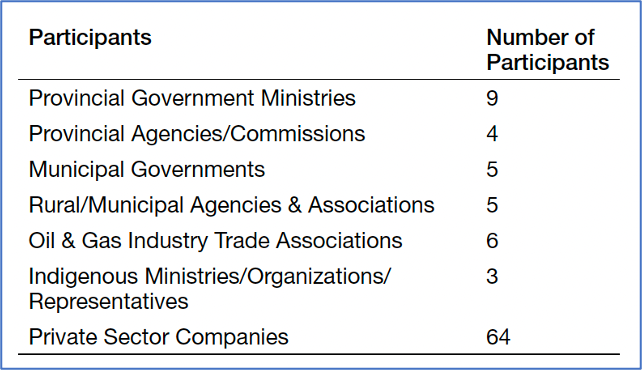

Despite some effort to broaden engagement, the development of the MAS was mostly faithful to the unfortunate but long-standing secretive approach to policymaking in the unfunded closure liability context. Cabinet officials (e.g., ministers and their department staff) were directly involved in organizing the consultation process, with a small selection of government officials, industry lobby organizations, oil and gas corporations, engineers, municipalities, surface rights associations, and landowners. Approximately 200 participants from 97 entities were involved (at 14; see Table 1, below).

Table 1: Participants (entities) in the MAS

For a policy review whose stated intention is to address the financial and environmental risks of unfunded closure liabilities and restore public confidence in industry and the provincial government (at 16), a non-public process such as this only reinforces concerns about regulatory capture by industry interests and does little to restore trust and confidence – trust which the MAS (in somewhat vague terms) admits is broken (at 5).

One important and notable change is that, unlike typical past AER consultations on liability management, this one did include representatives of the Rural Municipalities of Alberta (RMA). The results underscore the value and necessity of including a broader set of impacted groups but also highlight why the Alberta government and industry generally refuse to do so. The RMA quickly identified problems with the MAS and published a response document that raises concerns, among other things, about “unfounded assumptions” (at 2), that “flaws in the process directly contribute to the questionable credibility of the [MAS]…” (at 3) and “most of the goals in the report are heavily focused on changes to broadly benefit industry, with no consideration of risks or impacts on other stakeholders.” (at 11) Although the RMA was included in the process, the MAS generally ignores the information and perspectives the RMA provided.

By way of comparison, one of us participated in the Alberta Utilities Commission’s (AUC) government-mandated review of closure liability requirements for renewable energy projects. Those hearings and the AUC’s Module A Report provide a useful contrast to the MAS. With respect to the AUC’s hearings, written submissions were broadly encouraged from interested parties, including members of the public, who were also given an opportunity to appear before the AUC. The AUC also commissioned several expert reports. All of these submissions and reports are publicly available on the AUC’s website upon registration with their filing system (see Proceeding 25801, which contains over 300 filings).

The resulting AUC Module A Report is a good example of the value of independent agency analysis. Issues were addressed clearly and sequentially, and findings were supported with reference to the record. For example, and bearing in mind that the inquiry was spurred in large part due to concerns over agricultural land, after reviewing the submissions the AUC observed:

-

- There are many drivers that contribute towards the loss of agricultural land besides power plant development… From 2019 to 2021, the largest driver of agricultural land loss was expansion of pipelines and industrial sites (non-solar or wind), which accounted for 1,859 hectares and 1,607 hectares of land loss, respectively. In comparison, solar generation projects resulted in the loss of 833 hectares of agricultural land and wind turbines resulted in a loss of 205 hectares (1.6 sections of land) during this time… The total loss (gross) of agricultural land by all drivers during that period represents 0.05 per cent of the 2019 agricultural inventory. The Commission recognizes that certain areas of the province have experienced a higher percentage of land loss due to power plant development. One report indicated that in the Lethbridge-Medicine Hat economic region,27 close to half of the agricultural land loss in that region between 2019 and 2021 was due to solar generation development.28

(AUC Module A Report, at para 82. Footnotes 27 and 28 refer to a report submitted to the AUC and publicly available as an exhibit).

The MAS, on the other hand, is the kind of policy report that results from a process unconstrained by the administrative law principles that bind formal public inquiries and independent agencies like the AUC, including impartiality and responsive justification (Canada (Minister of Citizenship and Immigration) v. Vavilov, 2019 SCC 65 (CanLII) at para 133). While some facts and numbers are substantiated (e.g., well counts by status, at 11), many statements and conclusions are unsubstantiated or even contradictory.

For example, the MAS asserts that “multiple facets of the province’s vital energy industries have evolved more rapidly than stakeholders, participants, regulators, and policymakers have been able to adapt and respond” (at 4 and again at 13). But even a cursory familiarity is sufficient to know that nothing has been surprising about the inactive and orphan site inventory over the past three decades: it was and remains the most predictable and consistent trend emanating from a liability management regime devoid of closure deadlines or meaningful security requirements.

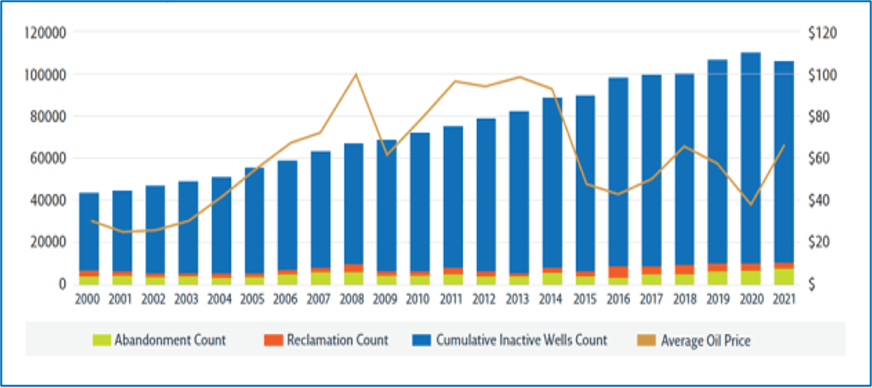

As illustrated by the Auditor General in their 2023 report, and a decade ago by the AER when it launched its Inactive Well Compliance Program (in 2015; see here and here), the steady growth of the inactive well inventory was among the few constants in the past twenty-five years (see Figure 1). As we’ve noted before, this figure also betrays the lie that the problem was caused by low oil prices. The inactive inventory grew whether commodity prices were low or high (the same is true for natural gas prices, which collapsed in 2009, well after the trend in growing inactive inventory was set).

Figure 1: Closure Activity and Growth of Inactive Wells with Oil Price

(Source: Auditor General of Alberta, 2023)

The MAS acknowledges this happened without acknowledging this was intentional regulatory design forcefully lobbied for by industry. The MAS puts it this way:

Historically, Alberta’s regulatory framework has not included fixed timelines for closure compliance. If the asset does not pose an immediate environmental hazard, the mineral license fees, municipal taxes, and surface leases are paid, and the licensee is not insolvent, there is no deadline for closure.

Positive aspect: This closure flexibility allowed companies to reinvest more cash flow from production, driving growth in the economy through investment, employment, taxes, and royalties.

Negative aspect: However, this also led to companies delaying closure activities. As cash spent on closure does not yield returns, there has been a default behavior by some licensees to postpone these efforts.

(MAS at 13, emphasis added).

Setting aside for the moment that municipal taxes and surfaces lease compensation are increasingly not being paid by industry (we return to this point when discussion section 5.1 of the MAS, below), this is a startling if also welcome admission: provincial energy officials (including the AER and its predecessors) designed a system that allowed companies to focus their resources on increasing production, so the (vast) majority did. The subsequent growth in closure liabilities was not just plainly foreseeable, it was the only plausible result. The basic deficiencies in the regulatory framework – the absence of closure timelines or some meaningful security requirement – have been known for at least three decades in Alberta, and yet they persist to this day.

Equally jarring, the MAS positions oil and gas companies as the hapless victim of external pressures and attacks, as if they were not aware that oil and gas are – and always have been – volatile commodities and non-renewable resources. The MAS attempts to rewrite the origin story of this crisis by totally ignoring the decades of intense industry lobbying and political influence in designing this failed liability management system. This alone significantly undermines the credibility of all the recommendations in the MAS because it fails to properly understand and account for the problem.

As another example, the MAS boldly asserts that the AER’s regulatory performance is “exemplary”:

Despite the growing number of non-commercial assets, Alberta’s regulatory compliance in protecting air, land, water, people, plants, and animals remains exemplary. Any leakage or spillage of hydrocarbons, produced water, or associated chemicals is addressed swiftly and thoroughly, regardless of cost. Incidents are immediately reported to the AER by operators or the public, with prompt action taken. (at 12)

Extraordinary claims demand extraordinary proof, but none is offered. If the MAS process included broader participation and some basic rules of evidence, such a bold statement could – and would – have been challenged. Consider, for example, the initially unreported release of toxic pollution from Imperial Oil’s Kearl oil sands site, which the AER did not even begin to investigate until many months later (for some commentary see The Alberta Energy Regulator and the Disclosure Without Delay Rule in FOIP and Administrative Penalties at the Alberta Energy Regulator: Regulatory Penalties for the Kearl Oilsands Leak).

Indeed, readers may recall that just a few years ago, the province’s Coal Policy Committee was deeply troubled to learn that “out that of about 25,000 respondents [to its survey], 85 per cent said they were not confident that the [coal] industry was being adequately regulated.” The problem is not that the public mistakenly believes the AER is ineffective or captured – it’s that the public is correct: the AER is ineffective or captured. One of us made a submission to the Coal Policy Committee intended to shed some light on this point:

…a close examination of the past fifteen years of environmental regulation in Alberta reveals an overwhelming pattern of regulatory failure. This examination includes over half a dozen independent expert reports, each of which has noted serious deficiencies in regulatory practice and design: inadequate environmental impact assessment (EIS) processes; deficiencies in assessing and managing cumulative effects; insufficient monitoring and enforcement; and inadequate bonding for reclamation and restoration. By and large, these deficiencies have been ignored or, as in the exceptional case of monitoring, addressed temporarily only. (submission of Martin Olszynski, at 1)

The AER’s regulatory performance has also very recently been called into question in peer-reviewed journals (see e.g., here and here). Suffice it to say, and as we concluded in How secrecy and regulatory capture drove Alberta’s oil and gas liability crisis, nothing short of an independent and transparent public inquiry with meaningful opportunities for fact-finding, investigation, and deliberation will ever restore the trust broken between industry, regulatory agencies, and the public. A review directed by Cabinet and overseen by an adviser and close political ally to the Premier with a selected group of participants whose deliberations were undertaken behind closed doors misses the mark entirely.

II. The Substance of the MAS

A. Recasting the Nature and Extent of the Problem?

As a starting point, it is remarkable that the MAS does not employ the long-standing and broadly understood terms and categories of oil and gas infrastructure as they appear in legislation and in numerous AER websites and publications. This is an odd choice for a policy roadmap that seeks to be the basis for sweeping legislative changes. Instead, the report’s central definition is for “mature assets”. While acknowledging the difficulties of bundling so much under one umbrella, it claims “a workable definition for a mature asset would include an oil and gas producing asset, which refers to a reservoir, field or well that has been producing for an extended period and is at a stage where production rates are declining, making it marginal or uneconomic to continue operation at present or at some point in the near future” as well as associated facilities (at 17).

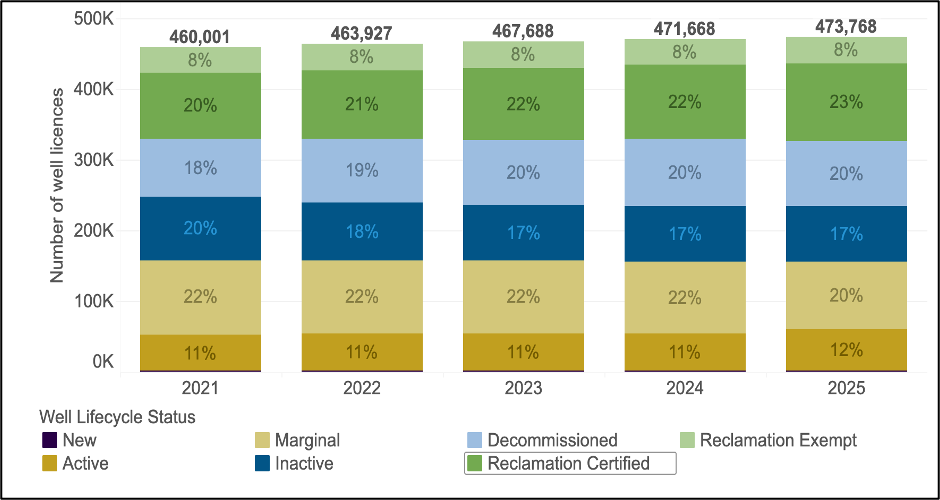

This new category of “mature asset” consequently bundles together marginal wells, inactive wells, and orphan wells, some of which might theoretically still be assets, with almost 100,000 decommissioned but un-reclaimed wells, which by virtue of their decommissioned status can only be liabilities (as one of us recently explained here). In Alberta, then, ‘mature assets’ outnumber ‘non-mature assets’ roughly five-to-one (see Figure 2), so the MAS will effectively be a new regulatory strategy for most of the conventional oil and gas industry.

Figure 2: Number of Licensed Wells in Each Stage of the Life Cycle

(Source: Alberta Energy Regulator)

In recasting the problem, the MAS manages to be both detailed and vague. It provides some specific facts in relation to quantifying the unfunded closure liabilities problem but then fails, or more accurately refuses, to clearly describe the actual extent of the problem. The salient facts provided on quantification are as follows:

- As of November 30, 2024, the AER reported 471,363 licensed wells in the province, representing about 9.5% of the global total.

- Alberta currently has 274,215 wellbores that are either marginal, inactive (non-producing), or decommissioned (wellbore decommissioned, reclamation incomplete, or not yet receiving a reclamation certificate) compared to almost 54,000 producing wells and almost 105,000 wells which have been successfully reclaimed.

- In addition to wellbores, AER reports that industry has built 38,553 production facilities, such as batteries and separators. As of the end of 2023, 7,525 (20 per cent) had been decommissioned but not reclaimed, 15,434 (27 per cent) were inactive, and 19,582 (51 per cent) were still in operation.

- To transport products to market, the industry has constructed 446,091 kms of flowlines and pipelines. By year-end 2023, 23 per cent had been decommissioned, 16 per cent were classified as “discontinued” or non-operating, and 60 per cent remained in service.

(MAS at 11)

While these facts are relevant to the problem, the MAS refuses to incorporate them into an calculation or estimate of total closure liabilities, claiming it would be “inappropriate to draw long-term conclusions regarding the number of mature assets requiring closure, the total closure liability, or the ability of current licensees to fulfill closure obligations without considering … key economic drivers” (at 24), which the MAS then declares itself as having been “designed to address” (at 24).

As we and others (e.g., Alberta’s Auditor General) have observed repeatedly, one of the most significant policy failures in the Alberta energy sector is the absence of a credible official estimate of total closure liability. A sound liability management framework cannot be built on inaccurate liability estimates or unknown amounts. The AER formerly produced a calculation of the total deemed liabilities every month as part of the Liability Management Rating (LMR) Results Report (the final LLR deemed liability was $36 billion in July 2024) but those estimates were calculated using average liability cost estimates set by Directive 011 that are known to be inaccurate (D11 was recently updated but only in relation to decommissioning (i.e., abandonment or plugging) costs, whereas remediation and reclamation costs appear to be the most underestimated). The AER official estimates hovered in the low to mid $30 billion dollar range since 2015, an estimate that has always excluded any and all pipeline segments. The AER has acknowledged the errors in these estimates, and the Auditor General has described many of them, but the public continues to receive conflicting and inconsistent estimates of total closure liability from the AER, the Minister of Energy and Minerals, and the Premier (see Waiting for a Credible Cost Estimate of Oil and Gas Closure Liabilities and the Problem with CARL for more details on this posted by one of us in May 2024).

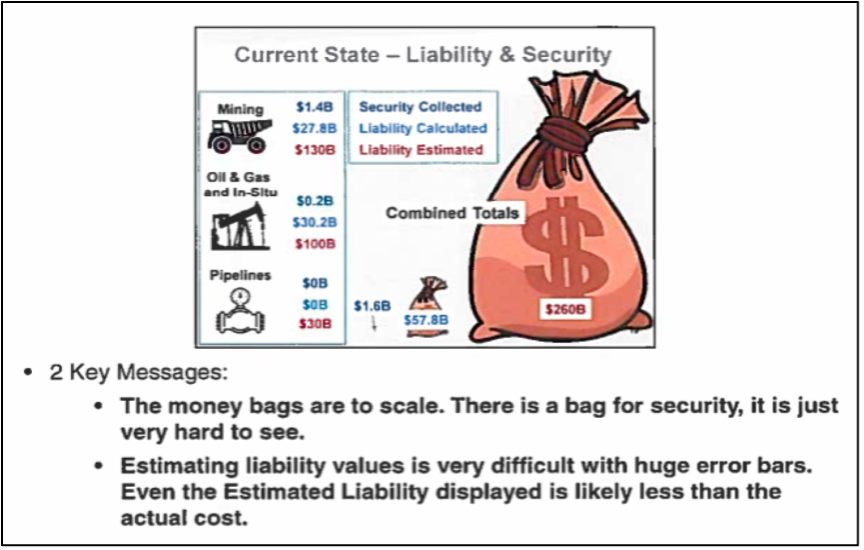

In 2018, a leaked internal AER presentation blew the roof off of published AER estimates. That presentation suggested that conventional liabilities are probably closer to $100 billion, pipeline liabilities are around $30 billion (based primarily on estimates of federally regulated pipeline liability) and $130 billion for oil sands liabilities, bringing the total to an eye-watering $260 billion (Figure 1). Every subsequent Freedom of Information (FOIP) request filed by one of us (Drew Yewchuk) and every regulatory review (e.g., the 2022 review of the Mine Financial Security Program) has tended to confirm, rather than refute, this figure. Adjusted for inflation, Albertan’s are currently staring down $320 billion in unfunded oil and gas closure liabilities.

Figure 3: Current State – Liability and Security (2018)

To put this figure in perspective, the MAS did see fit to publish the total resource revenue generated by oil and gas activity over the past 50 years: “Corrected for inflation using the Canadian Consumer Price Index changes from 1970 to 2024, the total non-renewable resource revenue collected since 1970 in current dollars is $553 billion” (at 23). In other words, on their current trajectory of falling onto the public purse, the oil and gas sector’s closure liabilities have the potential to erase roughly 60% of the non-renewable resource revenue collected by the province since 1970.

The salience and merit of the recommendations in the MAS are significantly impaired by the continued absence of any credible estimate of the cost of the unfunded inactive and orphan well closure liabilities problem.

B. Six Working Groups, 21 Recommendations

The MAS makes 21 policy recommendations, presented under six working groups. Because many recommendations are missing key details (e.g., six of the twenty-one recommendations (5, 7, 8, 10, 11, and 21) are mostly recommendations to establish more working groups), in the balance of this post we have not sought to provide a comprehensive summary but rather focus on those elements we find most promising or most problematic.

(1) Municipal Taxes and Rising Costs (section 5.1 of the MAS): This working group discussed the relationship between mature assets and unpaid surface compensation, unpaid municipal property taxes, and other fixed costs (such as the orphan levy), and the implications of those costs on the economic viability of mature assets. A recurring theme here is the assertion that “trust has been broken” (at 25). The MAS explains how landowners are required by law to host oil and gas operations, that surface lease payments used to be a “straightforward obligation”, but that now landowners face requests for reduced payments (or don’t get paid at all). The same basic dynamic applies to municipal taxes, with hundreds of millions in unpaid taxes owed to rural municipalities throughout the province. As we have been saying for years (as part of our criticism of the province’s asset-to-liability approach), the MAS acknowledges that “financially distressed companies often cannot retire mature assets, exacerbating tensions” (at 25).

As in other parts of the MAS, here again we find unfounded assertions that industry has faced unforeseeable and unfair challenges:

Despite record oil and gas production, significant royalty and tax contributions, and substantial job creation, some producers have struggled to meet financial obligations due to collapsing natural gas prices, limited access to capital, increasing costs from levies, carbon taxes, regulatory complexity, and mandated closure spending. These challenges forced many companies into bankruptcy or financial distress, prompting cost-saving measures, including non-payment of surface leases and municipal taxes. (at 25)

Again, even a cursory understanding of recent history is sufficient to negate the narrative being pushed here. First, and at the risk of repetition, surely just about everyone in the oil and gas industry has always understood that they deal with volatile commodities. Second, aside from the province’s own Specified Gas Emitter Regulation promulgated in 2007 (since replaced by the Technology Innovation and Emissions Reduction Regulation, Alta Reg 133/2019), which imposed an intensity-based carbon emissions cap on large emitters, carbon pricing generally was not introduced until long after the orphan and inactive well inventories exploded. Third, mandatory closure spending is an even more recent requirement, having been introduced in 2022 (and was bolstered with a $1 billion federal infusion). Fourth, limited access to capital was a direct result of the collapsing natural gas prices – banks stopped lending to natural gas producers who would not be able to repay loans. It was also a relatively recent phenomenon which became more acute after the Supreme Court of Canada’s 2019 Redwater decision (Orphan Well Association v. Grant Thornton Ltd., 2019 SCC 5 (CanLII)), which of course was itself driven by the reality that insolvent companies did not have the assets to cover their closure obligations. It is not rational or persuasive to blame the Redwater decision (at 12 and 16), as without Redwater producers would have likely dumped their worthless wells onto the OWA in even greater numbers. Rather, the Supreme Court’s Redwater decision likely saved Alberta’s regulatory system from immediate collapse. It was also a primary driver for the liability management changes yet-to-be fully implemented by Alberta in 2020 with the LMF.

Curiously, this section of the MAS fails to explain or even mention existing policy measures and legislation intended to address the problem of unpaid surface rents and taxes. For example, the AER’s assessment on companies who apply for new licenses, or to transfer existing licenses, includes whether there are unpaid municipal taxes above $20,000. This requirement was initially imposed on the AER in 2023 by the Minister of Energy in Ministerial Order 043/2023, wherein the Minister also directed the AER to require companies to reduce taxes payable below the threshold amount or give evidence of repayment arrangements with the municipality. Exceptions to this requirement were added following Ministerial direction in October 2024 (discussed in detail here).

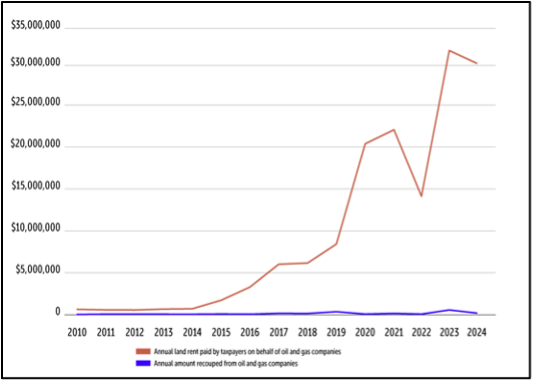

This section also fails to quantify the extent of existing government support for the industry. According to the RMA, unpaid municipal taxes amount to $253.9 million as of 2024. The province is also now covering an unprecedented number of delinquent surface lease payments (“The total paid by the government on behalf of delinquent companies since 2010 is nearly $150 million,” as recently reported by the Narwhal):

Figure 4: Land Rent Paid Annually by the Alberta Government on behalf of Delinquent Oil and Gas Companies (Source: The Narwhal)

The detailed recommendations here include: (1) addressing non-payment of municipal taxes, (2) reconstituting the Surface Rights Board, (3) reviewing AER license transfer mechanisms regarding closure liability funding, (4) recommendations to address surface lease non-payment, and (5) strengthening industry-municipality collaboration.

With respect to enhanced notification (recommendations 1 and 4), some additional transparency might be generated here, but without substantive legislated requirements this seems unlikely. Reconstituting the Surface Rights Board (SRB) seems odd given that Alberta only recently subsumed that Board into the Land and Property Rights Tribunal – and whether the flood of applications relating to unpaid surface lease payments goes to the new Land and Property Rights Tribunal or a reconstituted SRB does nothing to address the underlying problem that the “LPRT has seen a surge in disputes, handling 5,000 cases annually, with numbers expected to rise due to recent insolvencies” (MAS at 25). Reviewing the AER license issuance and transfer processes (recommendation 3) might be helpful if it leads to better transparency on how delinquent applicants and potential licensees are assessed, but the MAS provides the reader with no context on exactly what that process looks like currently, how non-transparent it is, and why too much AER discretion is a big part of the problem. The MAS proposed path forward also hints at a forthcoming demand for municipalities to lower their expectations: “Municipalities must balance financial sustainability with the realities of resource maturity, while producers face mounting fixed costs.” (at 26)

This part of the MAS strongly suggests the input of concerned municipalities was not followed, because the RMA directly opposed the “solutions” industry representatives were pushing (see the Rural Municipalities Response at 4). More generally, the failure of the MAS to meaningfully address rural concerns has been the source of much frustration on the part of landowners and the public more generally during the MAS townhalls currently being held across Alberta (for example see here for details of the September 9 event held in Warburg).

2) Resource Conservation and Enhanced Oil Recovery (section 5.2 of the MAS): This working group “examined the relationship between remaining oil and gas in mature conventional reservoirs and the economic conditions and fiscal regimes that could sustain production” (at 29). In many respects, this section repeats the same basic argument as section 5.1: oil production could be sustained if only all other costs could be reduced. It uses vague phrases like “Economic adjustments to taxes and/or royalties” (at 31) and “fiscal framework modifications” but the core proposal is to cut taxes, royalty rates, orphan levies, etc., or to provide public money to support new oil recovery technology for mature assets, in order to allow their owners to squeeze a few more drops of profit out of largely depleted and uneconomic sites.

The detailed recommendations here include: (6) developing financial models for mature fields, (7) establishing an EOR working group, (8) supporting innovation adoption through collaboration, and (9) supporting increased exploration and production in mature asset areas.

From the perspective of addressing the unfunded closure liability crisis, the recommendations from these two working groups (5.1 and 5.2) represent a massive moral hazard: “a situation in which a party is incentivized to risk causing harm because another party is obligated to remedy the consequences of the harm caused” (see also this short video explainer). Like the previous (notorious) R-Star proposal that was wildly unpopular with Albertans, these MAS recommendations effectively reward the oil and gas sector for failing to fulfill their legally required closure obligations.

Furthermore, if passed, it is hard to see how any remaining producers would ever take their closure obligations seriously. The precedent will be clear: continue to delay closure work until your assets are deemed mature, and then the Alberta government will reduce or even eliminate your debts (taxes, royalties, levies) owed to the public.

3) Economic opportunities (section 5.3 of the MAS): This working group “explored economic opportunities arising from existing mature conventional oil and gas assets and the regions that host them” (at 34). In essence, this section pitches ideas for Alberta to use more natural gas in order to increase natural gas prices for mature asset owners, e.g., to power artificial intelligence data centers (AIDC) (ibid) and to build out small-scale LNG production for regional use (at 35).

The detailed recommendations here include: (10) creating a gas gathering and transmission repurposing working group, (11) creating a working group to explore a regulatory framework for small-scale electricity generation, and (12) investigate or explore rural energy-based economic growth opportunities.

4) Shared Resources and Dedicated Closure Entities (section 5.4 of the MAS): This working group “reviewed the current state of decommissioning and reclamation (D&R) methods, processes, and techniques, focusing on identifying which operators are most effective in conducting D&R in a cost-efficient manner and understanding the reasons behind their success” (at 37). The section begins with an unnecessarily complex statement on why Alberta has an inactive and orphaned asset inventory problem:

Critics of the total spending on non-commercial producing asset retirement often argue that the responsibility lies solely with the oil and gas industry. However, the engagement process for the MAS has revealed that the situation is far more complex. Closure funds and spending are shaped by numerous factors, including commodity prices, capital markets, taxation, royalties, fixed costs, and operators’ operational, engineering, and financial capacity. The diversity among operators and assets results in varying closure liabilities and costs, especially for non-commercial assets created at various times with multiple owners with different styles of operating and commitment to environmental protection. When closure operations are not efficiently managed, operations and outcomes can become significantly more expensive. (at 37)

The “polluter pays principle” is actually very straightforward. As explained by the Supreme Court of Canada over two decades ago, the “principle assigns polluters the responsibility for remedying contamination for which they are responsible”: Imperial Oil Ltd. v. Quebec (Minister of the Environment), 2003 SCC 58 (CanLII) at para 24. The MAS confuses the simple legal issue of responsibility with more nuanced logistical questions. But here again, the MAS fails to provide the necessary historical context (noted above) or to substantiate the “numerous factors” that apparently cloud the issue. As one example, both here and elsewhere, the MAS suggests that liabilities are primarily a distressed producer problem: “The producers generating attractive returns on invested capital today are generally not the same producers that own many of the mature assets. No meaningful progress can be made on addressing mature assets until there is a broader understanding of who owns these assets and the financial challenges that many of these producers are facing” (at 21).

We agree that the public needs a better understanding who owns these assets and the financial challenges they may or may not be facing. We observe from the publicly available Inactive Well Licence List that 4 out of 5 of the companies with the largest inactive well inventories collectively own 29,997 inactive wells – or almost 40% of the entire inactive well inventory. Conversely, to the best of our knowledge, those under creditor protection or in bankruptcy (Long Run, AlphaBow and Sequoia) account for 7,509 inactive wells, or 9%.

Table 1: 20 Corporations with the Most Inactive Wells (Descending)

| Company Name | Company Code | Inactive Wells | |

| 1 | Canadian Natural Resources Ltd. | 0HE9 | 20,265 |

| 2 | Cenovus Energy Inc. | A5D4 | 5,450 |

| 3 | Long Run Exploration Ltd. | A517 | 2,705 |

| 4 | Obsidian Energy Ltd. | 0BP8 | 2,207 |

| 5 | Imperial Oil Resources Ltd. | 0007 | 2,075 |

| 6 | AlphaBow Energy Ltd. | A7H2 | 2,074 |

| 7 | Sequoia Resources Corp. | 0Z5F | 1,916 |

| 8 | Torxen Energy Ltd. | A7NW | 1,620 |

| 9 | Whitecap Resources Inc. | A5BE | 1,432 |

| 10 | Tourmaline Oil Corp. | A573 | 1,046 |

| 11 | Suncor Energy Inc. | 0054 | 990 |

| 12 | Blue Sky Resources Ltd. | A7XK | 939 |

| 13 | West Lake Energy Corp. | A7H7 | 929 |

| 14 | Baytex Energy Ltd. | 0RL9 | 922 |

| 15 | Cardinal Energy Ltd. | A6A7 | 917 |

| 16 | Paramount Resources Ltd. | 0AW4 | 856 |

| 17 | TAQA North Ltd. | A2TG | 853 |

| 18 | Texcal Energy Canada Inc. | A9CC | 814 |

| 19 | IPC Canada Ltd. | A868 | 766 |

| 20 | Harvest Operations Corp. | 0Z0H | 699 |

| Total inactive wells of the top 5 | 32,702 | ||

| Total inactive wells of the top 10 | 40,790 | ||

| Total inactive wells of the top 20 | 49,475 | ||

| Total inactive wells in Alberta (2024) | 78,230 |

This list of inactive wells demonstrates the problem with bundling all assets under the ‘mature asset’ umbrella. It may be the case that many mature assets are owned by barely solvent companies, but many inactive wells – that is wells that are no longer producing and need to be decommissioned and reclaimed – are owned by currently profitable companies who still have the money to pay for legally-required closure work. The ‘mature asset’ classification really obscures the picture here, and arguably allows profitable companies to benefit from policy recommendations that we are told are needed to help companies facing financial challenges.

Among such recommendations is a new approach in the form of dedicated ClosureCo’s and HarvestCo’s (it is not clear to us whether the ClosureCo and HarvestCo would be singular (one of each), or plural (enabling companies to create new ClosureCo’s and HarvestCo’s as deemed necessary)). A ClosureCo would be “a third party paid to assume the lease, liability and closure for a fixed sum from the current licensee” (at 37). The obvious problem is that private companies would only transfer assets to the ClosureCo where the fixed sum was less than the company’s own estimate of actual closure costs. A HarvestCo would squeeze the remaining drops of economic life from mature assets to pay for the closure work of those same assets. The reader struggles to understand the logic on how a HarvestCo could find economic gain out of assets left behind by companies as depleted assets.

This gap in the MAS fuels speculation and legitimate concern that foreseeable ClosureCo and HarvestCo funding shortfalls would be capitalized with public money and would accordingly amount to just another way to socialize the industry’s losses and defeat the polluter pays principle.

The detailed recommendations here included (13) a joint industry closure initiative, (14) enabling the expansion of HarvestCo entities, and (15) exploring updating insolvency law to capture the needs of closure and reclamation.

5) Closure liability funding alternatives (section 5.5 of the MAS): This working group “examined the current closure liability funding process and explored new financing instruments for reclaimed, existing, and new producing assets” (at 41).

This section repeats much of the same ahistorical narrative already discussed above, again without substantiation. However, it also discusses several “liability funding solutions” that in our view do merit further consideration, including “asset-specific closure financial instruments” that would “ensure closure costs are covered throughout an asset’s lifecycle, improving liquidity, and enabling smoother asset transfers” (at 42 and further elaborated at 43: “A new financial instrument attached to new assets upon creation, ensuring that the new assets will never be orphaned. This would ensure that closure liabilities are considered from the outset of asset development including future production operations.”). This approach should have been adopted when an early version of this ‘security-deposit’ was first considered by Alberta energy regulators in the mid-1980s. Today would be the next best option.

Also discussed is “establishing financial markets for methane mitigation” which could “incentivize the closure of high-emission assets while offsetting closure costs. These mechanisms, modeled on successful U.S. programs, could provide new ways of funding accelerated closure expenditures” (ibid). Although such an idea runs into additionality problems (offsets should only be granted for emissions reductions that are not otherwise required, whereas closure is already legally required), the emergence of studies suggesting that methane emissions from some abandoned and inactive wells may be seven times higher than officially estimated does suggest that this issue merits concerted attention and a tailored policy response.

The detailed recommendations in this section include: (16) enabling asset-attached closure funding mechanisms and establishing new working group for third-party end-of-life liability models, (17) examining the creation of a long-term liability indemnity fund for closed assets post reclamation certificate, (18) explore eventually requiring asset-attached closure funding on wells or assets that have been decommissioned for years but not reclaimed or where off-site contamination from those assets is present, and (19) exploring carbon credit markets for end-of-life closure funding on emitting assets.

6) Risk-based closure (section 5.6 of the MAS): This working group “assessed current closure

regulations to determine whether they are outcome-based, comparing them with regulations from other jurisdictions” (at 45). In a nutshell, the MAS invited industry to share its views about the stringency and associated costs of closure regulations, and the industry predictably responded that they are too stringent and too costly. The MAS calls on the AER to adopt new “Industry Recommended Practices” through Energy Safety Canada (formed in 2017 from the merger of Enform Canada and the Oil Sands Safety Association) (at 47).

Recognizing that much of this discussion would reasonably be understood as code for deregulation, the MAS cautions: “Participants acknowledged the political sensitivity surrounding the regulation of closure activities… There was a consensus that any changes must be accompanied by a clear demonstration of industry’s clear and public commitment to environmental stewardship, with a focus on achieving tangible improvements in closure funding and reclamation activities while continuing to minimize environmental risks” (at 46).

This neoliberal assurance that industry can regulate itself is exactly how the unfunded closure liability problem began in the early 1990s and has been allowed to build into the crisis Alberta faces today. The MAS fails to explain what a clear and public commitment to environmental stewardship would look like in this context, but we suggest industry has already squandered its opportunity to demonstrate that it can be trusted to complete closure work in the absence of stringent regulations.

This section’s detailed recommendations include: (20) mandating regulator engagement with the joint industry closure initiative process, and (21) forming working group to develop program details and operating mechanisms.

III. The Implementation of the MAS

At the September 9 Warburg MAS townhall referenced above, it was reported that the Alberta government has already accepted seven recommendations from the MAS for implementation:

1) Addressing non-payment of municipal taxes

5) Strengthening industry-municipality collaboration

7) Establish an enhanced oil recovery (EOR) working group

8) Support innovation adoption through collaboration

9) Support increased exploration and production in mature asset areas

10) Gas transmission repurposing working group

11) Regulatory framework for small-scale electricity generation

One recommendation has already been rejected: (“19. Explore carbon credit markets for end-of-life funding on emitting assets”). It was reported that all other recommendations in the MAS were “accepted for consideration and further developmental study”.

Many of the MAS recommendations will require legislative amendments to be implemented. But the AER has already begun to implement some recommendations that do not require new or amended legislation (a reflection of the discretionary nature of many existing rules). As one example, the Industry-Wide Closure Spend Requirement for 2026 (announced in Bulletin 2025-27) exempts some small dry gas producing companies (those identified as needing special regulatory assistance in the MAS) from the mandatory closure spend for 2026. The AER says the “exemption is an exceptional circumstance resulting from continued low natural gas prices”. However, as the MAS notes, natural gas prices collapsed “over the past 15 years” (at 12). A person might reasonably conclude this is more of a permanent change to the mandatory closure spend program.

IV. Conclusion

The MAS is less a strategy and more like smoke and mirrors (SAM) to distract and conceal the origins of the closure liability crisis in Alberta’s conventional oil and gas sector. Even worse, if implemented the MAS recommendations would reward the industry that neglected its closure obligations with new financial benefits and relaxed regulatory requirements, all of which represents a massive moral hazard and a socializing of losses.

The MAS is also unpersuasive in its attempt to rewrite the origin story here. This is perhaps the most remarkable thing about the MAS: its apparent obliviousness to the fact that the origins of Alberta’s closure liability crisis at the hands of the government and industry are well understood and documented. In addition to our own research published through the University of Calgary’s School of Public Policy, investigative reporting in the Globe and Mail from late 2018 still provides the most objective and frank explanation of the problem to this day – a “risky bet” that keeps being made, again and again, at the expense of all Albertans:

In the oil patch, pliant regulators have enabled well-known companies, including Husky Energy Inc., Enerplus Corp. and others, to foist cleanup costs onto small companies that are buying up the distressed wells of those bigger players. In some cases, those smaller players are purchasing the assets even though they are unable to secure financing from major banks.

The risky bet is that natural-gas prices will rebound and deliver payoffs big enough to generate profits while also funding the cleanup of old wells as they peter out.

But the gamble has stirred a backlash in the industry. It has also angered landowners who complain of being shortchanged on lease payments from energy companies. And ultimately it has left taxpayers to shoulder a financial and environmental mess. In Alberta, a string of corporate bankruptcies has already pushed the number of defunct well sites to 4,349, up from 545 in 2014, necessitating a $235-million loan from the provincial government last year to shore up the fund set aside by industry to pay for cleanup. And that count does not yet include any of Sequoia’s wells…

The deal-making has been heady. Data compiled by The Globe from Canada’s three westernmost provinces show that at least 140,367 oil and gas wells have changed hands since 2015, the year after the price crash took hold. Of those, almost half were transferred to companies with subpar financial status as determined by Alberta’s regulator. Buyers include holding companies and firms that are anything but household names, such as ACCEL Canada Holdings Ltd., Acquisition Oil Corp. and COR4 Oil Corp. Many are small firms with only a handful of employees and were created in the past few years.

In 2016, the AER did, in fact, toughen rules, essentially requiring that the value of a company’s assets be at least twice the deemed liabilities upon completion of an acquisition. But the standard has been only loosely enforced. Meanwhile, some companies have gone to great pains to simply circumvent the scrutiny. Perpetual Energy set up a structure that allowed it to do just that, Sequoia’s bankruptcy trustee alleges in the suit filed against Perpetual and Ms. Riddell Rose. Rather than transferring assets to Mr. Wang’s outfit, the suit alleges, Perpetual sold shares of an established subsidiary that held the wells…

(Jones, J., Lewis, J., D’Aliesio, R., & Wang, C. (2018, November 23), “Hustle in the oil patch: Inside a looming financial and environmental crisis” The Globe and Mail)

Alberta’s unfunded closure liabilities in the conventional oil and gas sector have been a known problem for almost 50 years. Over that time, regulatory officials and industry have proposed and implemented various measures, few of which have been effective because of three chronic and fundamental deficiencies in the regulatory framework: (1) a lack of transparency that impairs accountability and public scrutiny for closure liability decisions; (2) too much reliance on discretionary power to implement legal requirements that would mitigate and address closure liability (e.g. security requirements); and (3) too much industry influence in the design of a liability management regulatory framework. The MAS acknowledges some of the transparency problem, but otherwise offers nothing substantive to address these fundamental deficiencies in Alberta’s liability management framework. On the contrary, it proposes to further entrench industry influence.

As the old saying goes, where there is smoke [and mirrors], there is fire. Nothing short of a full and proper public inquiry into the origins of, and risks associated with, Alberta’s unfunded closure liability problem will put Alberta on a path towards effective solutions that prevent liabilities from being further socialized to the public.

This post may be cited as: Martin Olszynski, Drew Yewchuk, and Shaun Fluker, “The Mature Asset Strategy for Alberta’s Oil and Gas Closure Liability Crisis: Where there is Smoke [and Mirrors], there is Fire.” (20 September 2025), online: ABlawg, http://ablawg.ca/wp-content/uploads/2025/09/ Blog_MO,DY,SF_MatureAssets.pdf

To subscribe to ABlawg by email or RSS feed, please go to http://ablawg.ca

Follow us on Twitter @ABlawg