By: Drew Yewchuk

PDF Version: The Sequoia Bankruptcy Part 1: The Motion to Strike and the Interveners

Cases Commented on: PricewaterhouseCoopers Inc v Perpetual Energy Inc, 2020 ABQB 6 (CanLII) and PricewaterhouseCoopers Inc v Perpetual Energy Inc, 2020 ABCA 417 (CanLII)

The Orphan Well Association (OWA) was back in court on December 10, 2020 for the appeal of PricewaterhouseCoopers Inc v Perpetual Energy Inc, 2020 ABQB 6 (CanLII). The OWA is concerned about the interpretation of the Supreme Court’s decision in Orphan Well Association v Grant Thornton Ltd, 2019 SCC 5 (CanLII) (Redwater), and specifically whether the finding that abandonment and reclamation obligations (ARO) are not “provable claims” in bankruptcy implies that ARO are not “liabilities” for the purposes of determining the financial situation of a corporation and hence whether a corporation is solvent.

The Redwater decision concluded that a trustee for a bankrupt oil and gas company had to use the bankrupt estate’s assets to pay for the ARO of non-producing wells, and could not “disclaim” them. Redwater started as a bankruptcy case under the name Redwater Energy Corporation (Re), 2016 ABQB 278 (CanLII). (I recommend Nigel Bankes’ earlier posts on the Queen’s Bench decision and the Court of Appeal decision in Redwater, and Jassmine Girgis’s post on the Supreme Court decision for a complete background.)

The PricewaterhouseCoopers cases relate to the transactions that preceded the bankruptcy of Sequoia Resources. Sequoia had insufficient assets to cover their ARO when they entered bankruptcy, and they left more than 2000 wells to the OWA. “Sequoia” refers to the redwood tree, so in a strange coincidence, this sequel to Redwater is about a company named for redwood.

The background facts for the PricewaterhouseCoopers cases involve a complex set of nested corporate transactions and multiple regulatory systems. The Perpetual Group is a group of companies (Perpetual Energy Inc, Perpetual Operating Trust, and Perpetual Operating Corp), which held non-producing wells with large ARO. Perpetual moved ownership of wells with roughly $200 million in ARO and municipal tax liabilities and about $7 million in valuable assets into a corporation called Perpetual Energy Operating Company, and then sold the Perpetual Energy Operating Company to 1986114 Alberta Inc., a company wholly owned by Kailas Capital Corp, for a dollar. The Perpetual Energy Operating Company thereby became solely responsible for the Perpetual group’s expensive ARO which were removed from the Perpetual Group’s balance sheets. After the sale, Perpetual Energy Operating Corp. changed its name to “Sequoia” and went bankrupt about 17 months later. The buyer, Kailas Capital Corp, was owned by Mr. Hao Wang and Mr. Wentao Yang, who are not involved in the PricewaterhouseCoopers litigation, but are being sued by Shanghai Energy Corporation in a separate lawsuit related to Sequoia transactions. No decisions have been published in relation to that lawsuit.

The Alberta Energy Regulator (AER) has a set of regulations and directives meant to prevent bankruptcies from leaving large amounts of wells to the Orphan Well Association. I will refer to that set of regulations and directives as the ARO management system. The basic approach is that the AER tries to ensure that all companies holding oil and gas licenses have sufficient assets to cover their ARO liabilities at all times. The Sequoia bankruptcy and the transactions that preceded it represent a failure of the ARO management system, as something clearly went badly wrong in order for those 2000 wells to end up with the OWA. Although it is not immediately obvious, PricewaterhouseCoopers Inc v Perpetual Energy Inc is the AER trying to enforce ARO management system.

PricewaterhouseCoopers (the Trustee) is the trustee in bankruptcy for Sequoia, and is suing the Perpetual Group and a former director of Sequoia in relation to the sale of assets from Perpetual to Sequoia. The Trustee is acting primarily for the AER, and attempting to unwind the transfers or obtain a payment from Perpetual (or the former Sequoia director) in order to pay for as much of the Sequoia ARO as possible. The Trustee is attempting to protect the ARO management system, an inversion of Redwater, where the trustee was attempting to evade Alberta’s ARO management system.

There are two views of this situation: the Trustee takes the position that the Perpetual Group transferred non-producing wells to Sequoia knowing that Sequoia would carry the Perpetual Group’s ARO into bankruptcy, allowing the surviving members of the Perpetual Group to evade the ARO management system. The view of the Perpetual Group is that the Sequoia was merely an ambitious corporation that believed it would be able to handle the ARO as cheaply as possible, and that Sequoia was a victim of unexpectedly low gas prices during a downturn. What the two views have in common is that the Perpetual Group used the transfer to dispose of a large amount of ARO – the dispute is over whether the transfer was illegitimate in any way.

One strange analogy to the strategy the Perpetual Group used to dispose of their ARO is the Double/Split Person scheme identified as a pseudo-legal argument when used by individual persons in Meads v Meads, 2012 ABQB 571 (CanLII) (at paras 417-446). That pseudo-legal scheme consists of pretending that an individual has divided themselves into two legal entities and that one has all the liabilities and legal obligations, and the other one (the actual physical person) can walk away with the benefits and assets. The difference, of course, is that this split person strategy is well established in law for corporations – so here it may be a legitimate business strategy and not something that will get you labelled a vexatious litigant.

There are already six published decisions in the PricewaterhouseCoopers Inc v Perpetual Energy Inc saga, and there will be many more. This post covers two decisions: the application to strike, and the applications to intervene in the appeal of that decision.

The Application to Strike

The first decision was PricewaterhouseCoopers Inc v Perpetual Energy Inc, 2020 ABQB 6 (CanLII), a decision of Justice D.B. Nixon on applications to strike. The main claim in the litigation is being brought by PricewaterhouseCoopers (the Trustee) against the Perpetual group. The Trustee is seeking an order declaring a transfer of assets void as against the Trustee or judgment for $217,570,800, being the amount the Trustee considers to be the difference between the value of the wells received by Sequoia and the money paid by Sequoia (at para 3). In other words, the Trustee claims that $217,570,800 of ARO was improperly shifted into Sequoia. The Trustee seeks these remedies under four different causes of action: (1) a claim of transfer at undervalue under the Bankruptcy and Insolvency Act, RSC 1985, c B-3 , (2) an oppression claim under the Business Corporations Act, RSA 2000, c B-9, (3) a claim for equitable rescission on the grounds of public policy or statutory illegality, and (4) a claim against the former Sequoia director for breach of fiduciary duty (at para 5). The Perpetual Group applied to strike each of them.

The Trustee is representing the groups who had an interest in Sequoia at the time of its bankruptcy: in this case, the AER and municipalities owed taxes by Sequoia (at paras 204-211). If any individuals or private corporations were owed money by Sequoia, they do not seem to be involved in the bankruptcy process. One source of confusion here is that the Trustee is normally understood as protecting the interests of the bankrupt’s creditors, but in this case the Trustee is acting to recover money for ARO, and the Supreme Court’s Redwater decision is clear that the AER is not a creditor for the purposes of ARO (at para 225).

First, Justice Nixon considered the claim of transfer at undervalue. This is a claim that the transfer was done prior to bankruptcy for the benefit of someone other than Sequoia. The key question is whether the parties to the transfer were “related persons” or dealing at “arm’s length” within the terms of the Bankruptcy and Insolvency Act, RSC 1985, c B-3. The decision includes a thorough discussion of the law of “arm’s length” transactions under the Bankruptcy and Insolvency Act. Justice Nixon determined that the issue could not be resolved in a summary process as a more complete record would be necessary, as well as a consideration of the credibility of witnesses (at paras 98-99, and 107-110).

Next, Justice Nixon considered the oppression claim. An oppression claim is a broad type of claim allowed by section 242 of the Business Corporations Act, RSA 2000, c B-9. An oppression claim (or oppression remedy) allows a court broad powers to undo corporate conduct that “is oppressive or unfairly prejudicial to or that unfairly disregards the interests of any security holder, creditor, director or officer.” Justice Nixon started by considering whether the Trustee was a proper person to act as a “complainant” for an oppression claim. “Complainant” is defined in section 239 of the Business Corporations Act (at paras 126-137). Ultimately, Justice Nixon determined that based on the Supreme Court’s decision in Redwater the ARO are “not a liability for purposes of the Oppression Claim” (at para 225). Since the AER is not a creditor, the Trustee should not be granted complainant status under the Business Corporations Act, and that therefore the oppression claim disclosed no reasonable claim and should be struck (at paras 236-241).

The Trustee also challenged the transfer as being void for statutory illegality and violating public policy. The Trustee alleged that the transaction had been set up to have Sequioa retain a 1% interests in valuable oil and gas assets in order to dodge the ARO management system (at para 261). This is an allegation that the Perpetual Group intentionally structured the transaction to get through a loophole in the ARO management system. Justice Nixon struck this claim for disclosing no reasonable cause of action (at paras 281-284). Justice Nixon also considered and struck claims against the former Sequoia director for breach of fiduciary duty, again partially based on Justice Nixon’s reading of Redwater (at paras 285-372). Ultimately, only the claim for an alleged transfer at undervalue pursuant to the Bankruptcy and Insolvency Act was not struck.

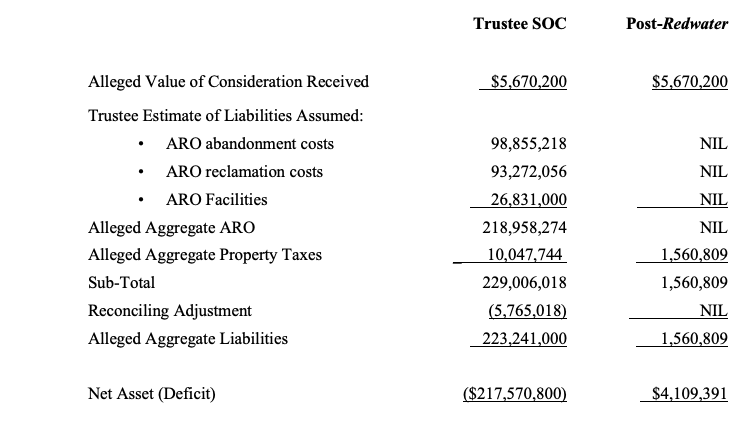

The impact of the interpretation of Redwater taken in this case is best shown by two paragraphs of the decision.

[368] My conclusion is supported by the financial component of the “Value and Consideration” in respect of the Asset Transaction. That financial result is as follows (see the “Post–Redwater” column):

[369] In effect, the decision in Redwater extinguishes the Trustee’s assertion that the Asset Transaction resulted in a significant net deficit. This “Post-Redwater” determination further demonstrates that there is no merit to the Director Claim insofar as it was premised on the ARO being a liability. Accordingly, I summarily dismiss the Director Claim under Rule 7.3(1)(b).

What this says is that the impact of Redwater is that ARO do not exist for financial purposes, and that parties dealing with oil and gas companies can ignore ARO costs entirely because ARO are not “claims” or “liabilities” and therefore should not show up on a balance sheet. The Supreme Court’s finding in Redwater was that ARO are not “claims” or “liabilities” because they are obligations arising under provincial laws of general application, and of greater importance than regular claims or liabilities (2019 SCC 5 (CanLII), at para 160). The impact of Justice Nixon’s understanding of ARO seems to be the reverse of the policy outcome in the SCC decision in Redwater and a repeat of the findings of the Queen’s Bench in the initial Redwater Energy Corporation (Re), 2016 ABQB 278 (CanLII) that the Supreme Court overturned.

The OWA and Industry Applications for Intervener Status

The Trustee appealed Justice Nixon’s decision. PricewaterhouseCoopers Inc v Perpetual Energy Inc, 2020 ABCA 417 (CanLII) is a decision on two applications to intervene in the appeal. The first application to intervene was from the Orphan Well Association and the second was a joint application by Canadian Natural Resources Limited (CNRL), Cenovus Energy Inc. and Torxen Energy Ltd. (at para 2). All the proposed interveners have a similar interest – if companies like Perpetual succeed in ditching their reclamation liabilities to somebody else, the proposed interveners would be that somebody else. The OWA is responsible for cleaning up orphaned wells (at para 15) and is funded by an orphan fund levy paid by industry. The other interveners

are a sample of those who pay the levy. CNRL holds the most licenses from the Alberta Energy Regulator (“the Regulator”) for wells located in Alberta and is accordingly the largest contributor to the levy, more than quadruple the next largest licensee. Cenovus holds several licenses and is a significant contributor to the levy. Torxen is an exploration and production company and maintains the second most licenses for wells in Alberta. Its small size relative to CNRL and Cenovus results in it bearing a greater percentage of the impact in relation to the levy. (at para 16)

The OWA is intervening specifically to challenge Justice Nixon’s “conclusion that ARO need not be considered by directors and officers in the discharge of their statutory and fiduciary duties, and that it is not something the Court should consider with respect to the oppression remedy” (OWA Factum). In seeking leave to intervene, the OWA also wrote:

Upon learning the details of the Transaction, the OWA became concerned because it appeared as though the Transactions were concluded for the express purpose of avoiding municipal taxes, and abandonment and reclamation obligations associated with the Goodyear Assets, and the Transactions appeared to have been carefully engineered to avoid the requirements of approval from the AER. The effect of the Transactions was to move significant regulatory obligations to Sequoia, a company with limited assets that has no ability to perform the obligations. This created a high likelihood that the Goodyear Assets would be required to be abandoned and reclaimed by the OWA. (para 12, OWA Brief)

Justice Rowbotham granted the OWA and the industry interveners leave to intervene (at para 30-31).

There also appears to have been an attempt by some municipalities to intervene based on a concern that the PricewaterhouseCoopers decision would impact municipalities trying to recovery taxes from oil and gas producers (see paras 50-61 of the Brief of the former Sequoia Director on the application to intervene). The municipalities’ intervention application appears to have been withdrawn before the application was heard, as the municipalities do not appear in the decision.

Commentary and Conclusion

Justice Nixon’s interpretation of how Redwater impacts the understanding of ARO is on one hand, absurd – how can $218,958,274 of clean up costs for oil and gas equipment count for nothing on a balance sheet? On the other hand, it is surprisingly consistent with the wording of the Bankruptcy and Insolvency Act and the Business Corporations Act. That is because those statutes are entirely focused on financial debts to creditors, and say little to nothing about laws of general application. This opens the door to interpretations where general laws become meaningless and only debts owed to creditors count. In my view, the point of Redwater is that laws are more important than debts, and public regulators are more important than creditors.

PricewaterhouseCoopers is related to problems with AER enforcement , international finance in general, and allegations of misconduct by Kailas Capital. My focus is on Alberta’s ARO management system. Alberta’s ARO management system was designed to encourage oil and gas development by being highly flexible and requiring minimal security deposits. The flexibility in the ARO management system has allowed corporations to develop strategies to evade ARO, and the minimal security deposits means the ARO management system is unable to manage declines in oil prices. Sooner rather than later, Alberta must implement a new system to obtain greater security for ARO liabilities. The need for action on Alberta’s ARO problem has been discussed at length in previous posts. The AER has recognized the problem and intends to make some changes, though details are still lacking.

One interesting takeaway from the intervener decision in PricewaterhouseCoopers Inc v Perpetual Energy Inc is that the dispute about ARO is not just between environmentalists and industry, or rural Albertans with wells on their land and industry; it pits two sections of industry against each other. In the first camp are companies with large volumes of producing assets in Alberta (CNRL, Cenovus, Torxen) who pay most of the OWA levy and who have representatives on the board of the OWA. In the second camp are companies with fewer assets who are winding up their oil and gas business in Alberta and pinning their ARO liabilities on the first group on their way out the door. We have the Court of Appeal decision on PricewaterhouseCoopers Inc v Perpetual Energy Inc to look forward to, and hopefully major reforms to the ARO management system.

This post may be cited as: Drew Yewchuk, “The Sequoia Bankruptcy Part 1: The Motion to Strike and the Interveners” (January 18, 2021), online: ABlawg, http://ablawg.ca/wp-content/uploads/2021/01/Blog_DY_Sequoia_Part_1.pdf

To subscribe to ABlawg by email or RSS feed, please go to http://ablawg.ca

Follow us on Twitter @ABlawg