By: Drew Yewchuk, Shaun Fluker, and Martin Olszynski

Report Commented On: 2023 AER Liability Management Performance Report

PDF Version: Grading the 2023 AER Liability Management Performance Report

On December 5, 2024 the Alberta Energy Regulator (AER) published the 2023 Liability Management Performance Report (2023 Report). This is the second AER Liability Management Performance Report to the public on progress to reduce Alberta’s massive unfunded closure liability in the conventional (non-oil sands) oil and gas sector. We gave the 2022 Liability Management Performance Report a failing grade here because it offered little in relation to understanding whether industry performance was adequate and almost nothing at all about the AER’s performance. We note with disappointment that the AER has apparently removed the 2022 Report from its website, since historical comparison is also a method of measuring performance. The 2023 Report receives a slight improvement to a D grade because of enhanced data transparency, but the AER continues to offer little in terms of measuring effectiveness and performance in the administration of liability management.

An Overview of the Closure Liability Problem and the Liability Management Framework

Closure liability refers to the cost of abandonment (increasingly being referred to as decommissioning), remediation, and reclamation of oil and gas wells, pipelines, and other facilities on public and private lands in Alberta. Policy and regulatory failure over the last forty years allowed the problem to grow into a massive environmental and financial crisis. This policy failure includes the absence of a credible estimate of total closure liability. The AER produces a calculation of the total cost of deemed liabilities every month as part of the Liability Management Rating (LMR) Results Report ($30 billion in May 2024) but those estimates are calculated using average liability cost estimates set by Directive 011 (last updated in 2015) that contain major errors and rely on faulty information. The AER has acknowledged the errors, the Auditor General has described many of them, and private industry consultants maintain databases to create more reliable closure liability cost estimates for use in oil and gas asset sales. The public continues to receive conflicting and inconsistent estimates of total closure liability from the AER, the Minister of Energy and Minerals, and the Premier (see Waiting for a Credible Cost Estimate of Oil and Gas Closure Liabilities and the Problem with CARL for more details on this posted by one of us in May 2024).

In 2020, the federal government provided Alberta $1 billion to distribute to oil and gas companies for closure work (although $137 million of that money was returned unspent). In exchange for that funding, the Alberta government announced a new policy direction for the regulation of conventional oil and gas closure liability in the form of the Liability Management Framework. The Liability Management Framework has four components: (1) reduce the number of inactive sites with outstanding closure work; (2) assess applicants and existing licensees to ensure their solvency and operational record demonstrates an ability to meet closure and other regulatory obligations; (3) expand the mandate of Alberta’s Orphan Well Association to enhance its ability to undertake closure work for sites without a solvent owner; and (4) develop a regulatory program to address closure liability associated with legacy and post-closure sites for which there is no responsible owner.

For the most part, the AER is responsible for implementing and administering the Liability Management Framework. The Responsible Energy Development Act, SA 2012, c R-17.3, gives the AER its overall mandate, authority, and power to regulate the development of energy resources and closure work. More specific powers and legal obligations are set out in various other enactments. For example, with respect to pipelines these enactments include the Pipeline Act, RSA 2000, c P-15, and Pipeline Rules, Alta Reg 125/2023. These enactments also provide the AER with power to make rules with respect to liability management. Those rules are found primarily in two directives: AER Directive 067 – Eligibility Requirements for Acquiring and Holding Energy Licences and Approvals and AER Directive 088 – Licensee Life-Cycle Management. AER Manual 023 sets out and explains specific procedures used by the AER to assess liability risk of applicants and licensees, as well as implement minimum mandatory closure spending requirements on inactive sites.

The AER website is a labyrinth in terms of explaining how the regulator administers and implements liability management, with many pages conveying information in a manner that is duplicative, convoluted, and confusing (see e.g. here, here, here, here, here, and here). Perhaps the best place to start is the Liability Management page, which provides a very cursory description of the components of the 2020 Liability Management Framework. This page mentions that legislative amendments were required to implement the Liability Management Framework, including amendments to AER Directive 067 and the enactment of Directive 088, and provides links to other pages that give some explanation to specific aspects of liability management: holistic assessment and licensee capability assessment, licensee management program, inventory reduction program, and the license transfer process. All of these pages are also linked to the Liability Management Programs and Processes page, along with additional pages such as the Orphan Well Association, liability management rating and reporting, mine financial security program, and insolvency. We noted in our review of the website for this post, that sometime over the past year the AER removed dedicated links to information on security deposits and legacy and post-closure sites, for which a limited bit of information remains on the general Liability Management page. The AER website was also redesigned in December 2024 to improve accessibility on phone and tablet devices, but the redesign did little to improve this overall confusing structure of the AER website.

Collectively, the purported purpose of these requirements is to reduce unfunded closure liability in Alberta. To accomplish this, the requirements mandate an annual amount of spending by industry on closure work. They also provide the AER with the power to holistically scrutinize the financial and operational capacity of applicants for new licenses and existing licensees to perform closure work, and to control those risks by refusing to grant or transfer licenses or imposing conditions such as security deposits. The AER describes the licensee capacity assessment as the ‘backbone’ of the holistic approach:

The licensee capability assessment (LCA) is the backbone of our holistic assessment of companies throughout the energy development life cycle in the oil and gas sector. Introduced through Directive 088: Licensee Life-Cycle Management, the LCA considers a variety of factors to help us evaluate a company, including their financial and liability risk, their performance compared with similar companies, and other operations, closure, and administrative factors, with compliance history being considered throughout.

The information that feeds into the LCA comes from several sources, including financial information that companies are required to provide us through Directive 067.

(AER, “Holistic assessment and Licensee Capability Assessment”)

The AER has been gradually developing and implementing the Liability Management Framework, but five years after its announcement the framework is still incomplete. As well, the AER continues to make incremental changes to its liability management rules and directives that as a whole do not address the substantive causes of the unfunded liability problem or reduce liability. In October 2024, the AER published some proposed changes to its closure liability management directives, including Directives 067 and 088. Two of us commented on these proposed changes in The AER’s Proposed Amendments to Closure Liability Management Directives: Much Ado about Not Much, and concluded these were small improvements but largely insignificant without further revisions.

As it has developed, the key parts of the framework are the holistic assessment and licensee capability assessment, the closure spend quotas (which are set without sufficient planning to be effective), the closure nomination program, and an expanded role for the Orphan Well Association. Major parts of the framework are still missing, and key elements remain severely underdeveloped. The AER has not developed any approach for legacy and post-closure sites. The AER has not developed the ‘licensee special action’ component described in the 2020 government policy announcement, possibly because the policy instruction for that component was unrealistic. The October 2024 announcement proposed changes to Directive 068 in relation to security for closure liability, however none of this establishes an overall regulatory approach for collecting security. And worse, there is still nothing here to suggest security requirements will be imposed by legislation, rather than entirely at the discretion of the AER (which, as repeatedly demonstrated, is captured by industry). It remains impossible for the public to know exactly when and under want circumstances the AER requires security deposits from industry to meet closure liabilities and ensure regulatory framework avoids socializing the losses to the public.

Additional information collected by the AER to undertake its holistic assessment on companies who apply for new licenses, or to transfer existing licenses, includes unpaid municipal taxes above $20,000. This requirement was initially imposed on the AER in 2023 by the Minister of Energy in Ministerial Order 043/2023, wherein the Minister also directed the AER to require companies to reduce taxes payable below the threshold amount or give evidence of repayment arrangements with the municipality. Exceptions to this requirement were added following Ministerial direction in October 2024 (discussed in detail here). The most significant change here is that the AER may now approve transfers of oil and gas licenses out of the inventories of bankrupt companies so long as the transferee owes less than $20,000 in municipal taxes. One risk with these new exceptions is that this requirement no longer roadblocks the strategy of new oil and gas corporations being created specifically to absorb particular assets from bankrupt oil and gas corporations (as occurred with Manitok).

Finally, and of particular relevance to the grading of a performance report, we remind readers that the AER’s performance on implementing the Liability Management Framework has also been the subject of a report by the Alberta Auditor General in March 2023. ABlawg commented on this report here and here. One key finding of this report is an absence of meaningful transparency from the AER. This problem manifests in two ways: (1) a lack of external performance measures on closure work; and (2) failure to report meaningful information to people in Alberta. The absence of transparency makes it difficult for the public to assess the AER’s performance and to hold the AER accountable for its regulatory functions in this area.

Specific deficiencies noted by the Auditor General in how the AER reports its performance to Albertans include the following:

Specific goals to ensure accountability for results as it changes key parts of its liability management system have not been established. For example, what AER views as a reasonable and sustainable level of inactive closure liabilities given level of industry activity, economic factors, and other considerations? What is the current closure liability amount and what is an acceptable level? What does AER define as timely restoration of inactive sites and what is the goal for timeliness?

The Ministry of Energy and AER annual reports contain data about the amount of closure activity and spending in Alberta. However, they do not report on the total number of inactive sites in Alberta making it difficult for Albertans to assess if net progress is being made to reduce inactive sites.

AER lacks external performance measures to demonstrate whether its liability management programs are working. The lack of public reporting on performance measures with targets also makes it difficult for Albertans to know if risks are being adequately managed and that the cleanup being done is sufficient. Reporting on activity alone is not enough to effectively measure the performance and achievement, or lack thereof, of goals.

AER’s most recent estimates, at the time of writing, for industry-wide (active and inactive) closure liabilities in Alberta ranges from $30 billion for wells and facilities to $60 billion if pipelines and more recent information are included. …. AER also has not defined what it considers to be an acceptable and sustainable level of closure liability.

An overall liability estimate includes both active and inactive sites, where active sites may not need closure work completed for years. Contrasted with inactive sites that may require closure work sooner. Also, the potential financial risk to the public depends on who is responsible for the liabilities.

(“Liability Management of (Non-Oil Sands) Oil and Gas, Report of the Auditor General March 2023” at 22 – 23, emphasis added)

The 2023 Report on Liability Management

The foregoing discussion provides necessary context to grade the AER’s Liability Management Performance Report. As we noted last year, our primary observation with this Report is that it does not provide the level or content of transparency called for by the Auditor General. Moreover, the Report fails to achieve even the AER’s own description of its objective:

This report tracks industry performance as it relates to liability management and the impact of the liability management requirements over time. The purpose of this report is to improve transparency about industry’s management of conventional oil and gas liabilities and to develop performance measure baselines and ongoing assessments both of industry as a whole and licensees specifically. (at 1)

The Report remains largely a presentation of aggregate data on closure activity and liability risk allocation; albeit the 2023 Report is a more detailed and nuanced presentation than what was offered in 2022. However, the 2023 Report contains the same shortcoming of the 2022 report in that it fails to set out goals and other measures to assess the performance of closure activity. This is not a ‘performance report’ – it is another exercise in public relations. What follows are highlights of the four sections in the 2023 Report.

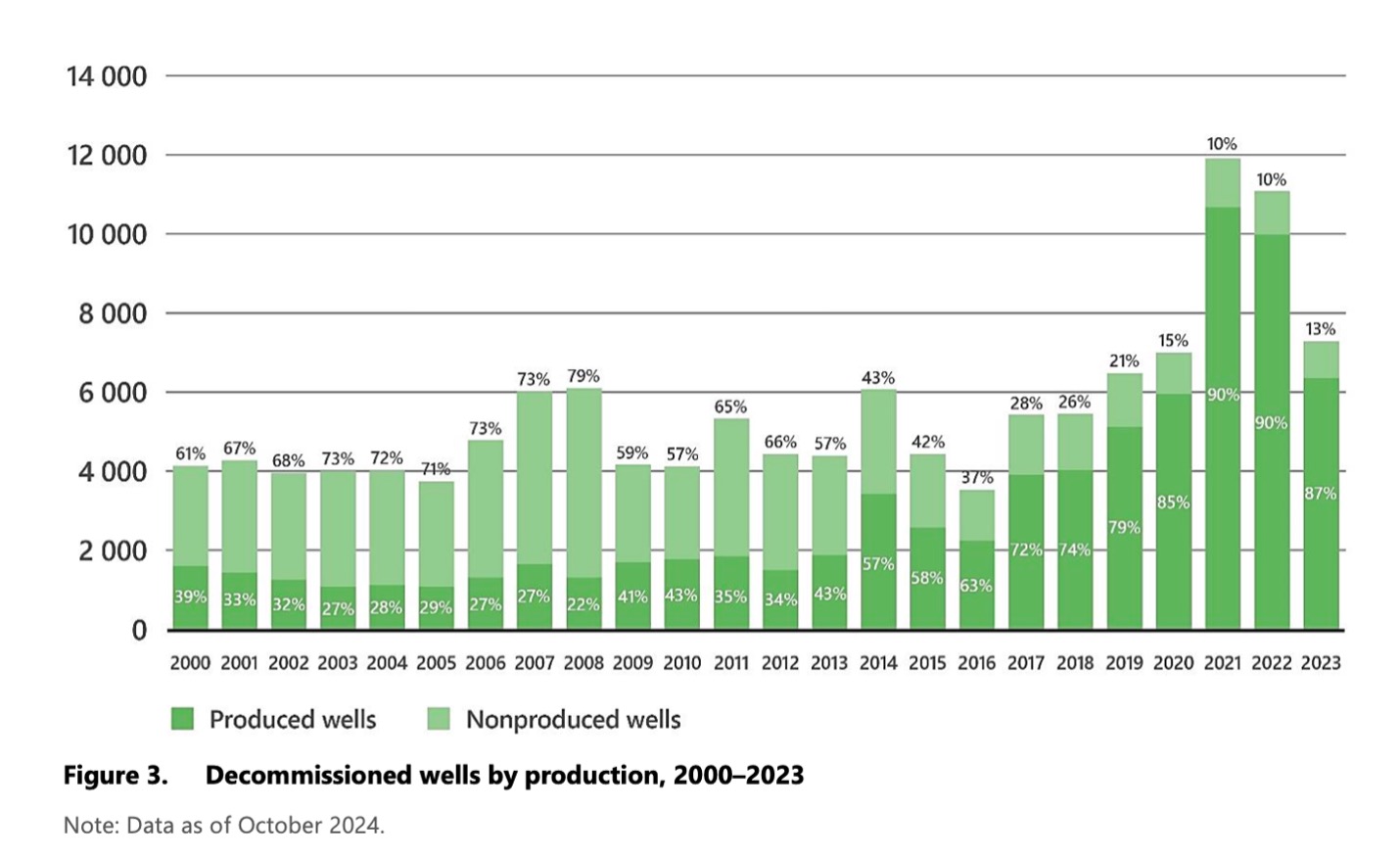

Section one: Conventional Oil and Gas Infrastructure provides data on the lifecycle status of wells, facilities, and (new for 2023) pipelines. Section one has more detail on a problem that had been previously reported by the Auditor General: from 2000 to 2013, 68% of the wells decommissioned had no reported production, making them less costly to decommission but not necessarily the most significant from a clean-up perspective. The 2023 Report indicates that industry is now decommissioning more produced wells since 2014 (at 3-4). The Report also discusses the age of the wells being decommissioned: “Of the wells decommissioned in 2023, 40% were inactive for ten or more years” and 10% had been inactive more than 20 years (at 4). “Approximately 36 000 wells inactive for ten or more years remain” (at 4, see figure 3).

39% of drilled wells in Alberta are either inactive or marginal producers, a tiny improvement compared to 40% in 2022 (at 5).

The addition of data on pipelines is also a welcome improvement in the 2023 Report. On pipelines, Alberta has around 267,000km of active pipeline and 71,000km of inactive pipeline. Inactive pipelines accumulated slower than inactive wells, growing from 2015 to 2021 before starting to slowly fall (at 6).

Section two: Estimated Liability and Licensee Capability continues to report estimated liability based on inaccurate data. Although this section properly notes that Directive 011, used to estimate liabilities, “was updated with well decommissioning costs, increasing the total liability to approximately $36 billion as of June 2024” (at 7, referring to the changes made by Bulletin 2024-16), the decommissioning cost estimates were understood to be less problematic than the reclamation cost estimates, which have not been updated. The improved estimates were also not applied to the estimated liabilities in the 2023 Report, so it contains inaccurately low liability estimates (at 7, figure 8). As we wrote about the 2022 report, “the AER continues to rely on – and publish – estimates that it knows do not provide an accurate picture of current liabilities.” It is not helpful for the AER to repeatedly publish information that they know is misleading, even if it comes with explicit cautions that the information is misleading.

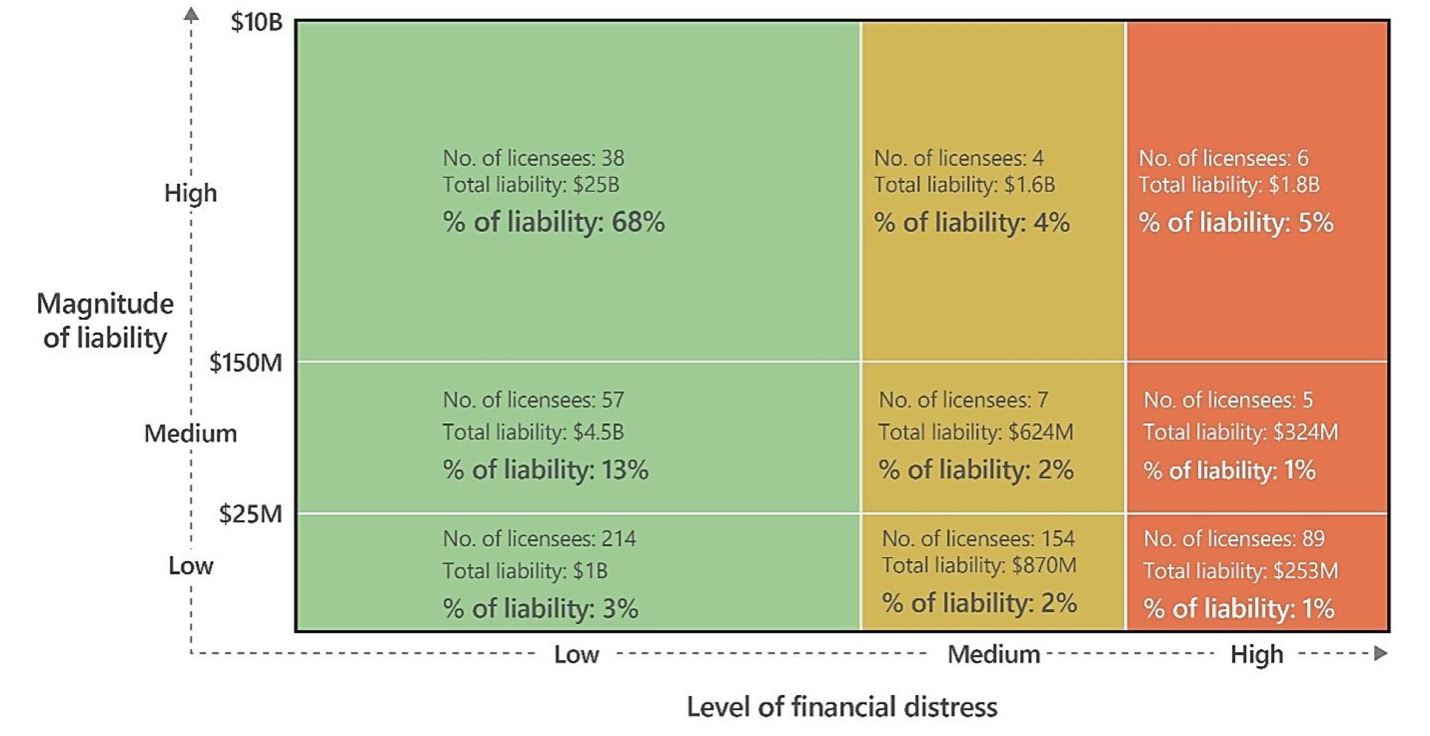

The 2023 Report provides a risk matrix on closure liability:

This table is the same format as presented in the 2022 Report.

As a performance measure, the table has limited utility, since some numbers are rounded to the nearest million dollars, other numbers rounded to the nearest hundred million dollars, and all the numbers are calculated on the basis of (grossly) underestimated liabilities. The 2023 Report does not assist the public in interpreting or giving meaning to the categories of low-medium-high for level of financial distress due to “confidentiality requirements”. It is also unclear to us how explaining the categories would violate the confidentiality of particular licensees. The Report provides no information whatsoever on how the AER has used or considered this information in its licensee capacity assessments or company-specific closure work quota requirements. We made the same observations with the 2022 Report, and curiously the 2023 Report offers no comparison with data in the previous report.

Here is what we observed by comparing the matrix table in the 2023 Report with what is in the 2022 Report. Liabilities held by licensees in the ‘low financial distress’ category increased around 22% (from $24.6 billion in October 2023 to $30.5 billion in October 2024). Liabilities held by licensees in the ‘medium financial distress’ category fell by 45% (from just over $5.5 billion in October 2023 to $3 billion in October 2024). Liabilities held by licensees in the ‘high financial distress’ category stayed fairly steady, between $2.5 billion and $2.3 billion (at 8). This suggests the new liability framework is having some success with companies that have financial issues but remain solvent but has not been successful for addressing the trickier problem of liabilities held by companies already approaching bankruptcy. In our view, nearly all companies in the ‘high financial distress’ category are bound for bankruptcy proceedings and the closure liabilities will end up with the Orphan Well Association, which receives only a fraction of the funds needed in annual levies from industry to pay for this closure work in a timely manner. Finally, with respect to this table, Albertans would be forgiven for assuming that the lion’s share of liabilities ($30.5 billion) is being taken care, when the opposite is true. Those liabilities are and will remain unfunded for the foreseeable future because the AER is still operating under the counterproductive and self-defeating assumption that security for liabilities should only be collected from financially distressed companies.

Data on transfers is included for the first time in the 2023 Report (at 9). The transfer data provides some useful information on how the AER has implemented the security deposit sections of Directive 088: Licensee Life-Cycle Management. When licenses were transferred from licenses in financial trouble to licensees in financially more stable positions, the AER generally took negligible security (below 1% of estimated inactive liability). When licenses were transferred from licensees in financially more stable positions to licensees in financial trouble, the AER generally took almost a quarter of the estimated liability cost (23% of estimated inactive liability). When licenses were transferred to ‘new’ licensees, the AER took 9% of the of estimated inactive liability. (at 9)

The transfers data is a welcome bit of transparency, but none of it offers a performance measure; particularly in relation to security requirements because the AER has yet to publish an overall regulatory approach to security and the regime is far too discretionary. The security collected as a percentage of liability appears to be far too low, in part because it is calculated on the basis of (grossly) underestimated inactive liability (one of us described the problem in detail in a May 2024 post), but also on its own terms: Collecting less than 9% of the estimated inactive liability cost for transfers to new licensees seems particularly troubling because of the huge volume (estimated at $906.2 million in liability) subject to transfers to new licensees (at 9).

Section three, Orphan Fund Levy, shows that, the OWA’s work spending on closure dropped from $185 million in 2022 to $149 million in 2023. The OWA’s spending from 2020-2022 relied on loans from the provincial and federal governments, those loans have been spent, and the OWA must now repay the loans. The OWA’s target closure date for the orphan inventory is 2036, and a faster rate of work would require a higher orphan levy. The 2023 Report lacks any notion of a performance measure on the effectiveness of the OWA because the report does not include information on target closure dates, and it also fails to provide any assessment on whether the annual levy imposed on industry is sufficient to meet those targets (See Drew Yewchuk’s post on the OWA and AER target closure dates for orphan, inactive, decommissioned oil and gas infrastructure.)

Section four, Inventory Reduction Program, shows spending on closure work dropped from $1.2 billion in 2022 to $1 billion in 2023 (at 14). This reduction roughly correlates with reduced spending from the Site Rehabilitation Program, funding provided by federal taxpayers (something the Report fails to mention). The 2023 Report includes several figures that set out closure spending by category of work (decommission, site assessment, remediation and reclamation), and by type of facility (at 14 – 16). The data shows an increase in reclamation certificates received by the OWA, which reflects the delay between reclamation work being done and the revegetation occurring necessary to receive the final reclamation certificate (see figure 15, page 13). Because the federal funding through the site rehabilitation program has ended, and the OWA has to decrease spending as it repays loans, closure spending in 2024 was likely around $900 million. Once again, as the Auditor General observed, we reiterate that reporting on activity alone is hardly a ‘performance report’.

Along with the report, the AER posted the interactive licensee dashboard and the interactive regional dashboard. Unlike the report, these dashboards provide information specific to licensees or regions of Alberta that was previously complicated or impossible to obtain from the AER. The information on the inventory of specific licensees will be useful to those monitoring and reporting on the closure liability situation.

Conclusion: Credible Liability Estimates and Goals for Liability Levels

The AER’s news release for the 2023 liability management report is positive spin on data that reveals two big problems. First, closure spending peaked in 2022, fell in 2023, and likely fell again in 2024. More closure spending from industry each year would be necessary to address the closure liability problem, but that is not scheduled to happen. Second, the liability management framework is having little success with the licensees in ‘high financial distress’ who cause the most short-term difficulties for landowners and municipalities.

In terms of data disclosure, the 2023 Report improves on the 2022 report. However, it is hardly an assessment of ‘performance’. The report does not contain any target levels or planned timelines for bringing unsecured active, marginal, and inactive closure liability down. This information is necessary to know what the current situation is, what the AER’s strategy is, and to assess whether the AER’s strategy is working. Without knowing what the goals of the liability management framework are, it is not possible to determine whether it is succeeding or failing, or if the framework has been rationally designed.

In late 2023 we published a critical evaluation of the legal and policy design of these new requirements (plus the orphan fund) in “A Made-in-Alberta Failure: Unfunded Oil and Gas Closure Liability”. Our analysis was informed by a historical review of Alberta’s approach to managing closure liabilities over the past 40 years in order to assess whether the Liability Management Framework is properly designed to achieve its objective of getting closure work done and ensuring the polluter — not Alberta taxpayers — pays for it. The conclusion of the study is that three factors that have contributed to Alberta’s historical failure to effectively manage closure liabilities remain problematic today in the design of the Liability Management Framework and its current legal and policy framework: poor transparency, excessive discretionary power exercised by the AER on a case-by-case basis in place of fixed rules, and a regulator captured by industry interests.

We maintain that these factors remain problematic with the AER and how it is administering the Liability Management Framework. Accordingly, we view the following as the three most pressing closure liability management issues the AER needs to address in 2025, listed below in the order they should be done:

(1) The extremely long running lack of transparency about the cost of oil and gas closure liabilities: The AER’s official liability estimate is too low, the AER knows it, and a sound liability management framework cannot be built on an inaccurate liability estimate. Well reclamation cost estimates must be updated and pipeline closure costs must be added to the total estimate.

(2) The lack of transparency on setting the mandatory closure spend and orphan fund levy: The AER must publicly set goals and timelines for addressing the closure liability problem so that the auditor general, the public, and the AER itself can assess whether the new framework is working as intended. The AER also continues to set the Orphan Well Levy in consultation with industry and out of the public view – recently sending us only a redacted version of the OWA Three Year Business Plan 2025-2028 that does not show any planned orphan levy amounts.

(3) The excessively discretionary approach to financial security collection: The AER needs to select a fixed approach that collects more security during transfers and as assets age that aligns with publicly stated goals for closure liability management.

For all these reasons, we grade the 2023 AER Liability Management Performance Report as follows:

D

This post may be cited as: Drew Yewchuk, Shaun Fluker & Martin Olszynski, “Grading the 2023 AER Liability Management Performance Report” (8 February 2025), online: ABlawg, http://ablawg.ca/wp-content/uploads/2025/02/Blog_DYSFMO_2023_AER_Grade.pdf

To subscribe to ABlawg by email or RSS feed, please go to http://ablawg.ca

Follow us on Twitter @ABlawg