By: Drew Yewchuk and Shaun Fluker

Report Commented On: 2024 AER Liability Management Performance Report

PDF Version: Grading the 2024 AER Liability Management Performance Report

In November 2025, the Alberta Energy Regulator (AER) published the 2024 Liability Management Performance Report (2024 Report). This is the third AER Liability Management Performance Report to the public on progress to reduce Alberta’s massive unfunded closure liability in the conventional (non-oil sands mine) oil and gas sector. We discussed the 2022 report here and the 2023 report here. In a positive change from earlier years, the AER has kept the 2022 and 2023 reports up on their website. While this allows the public to compare information in the current report with past years, it is noteworthy that the AER itself does not use the previous years to evaluate performance and the 2024 Report provides almost no discussion or analysis of the data set out in the report. This is one of the reasons why the 2024 Report receives an F grade.

An Overview of the Closure Liability Problem and the Liability Management Framework

Closure liability refers to the cost of abandonment (increasingly being referred to as decommissioning), remediation, and reclamation of oil and gas wells, pipelines, and other facilities on public and private lands in Alberta. Policy and regulatory failure over the last forty years allowed the problem to grow into a massive environmental and financial crisis. This policy failure includes the absence of a credible estimate of total closure liability. Despite updating the well decommissioning cost estimates in June 2024, the AER has still not updated the reclamation cost estimates even though the Regulator acknowledges those estimates are too low, meaning that the AER is deliberately producing an official conventional closure liability estimate ($36.6 billion) that is inaccurately low.

As we and others (most notably Alberta’s Auditor General) have observed repeatedly, one of the most significant policy failures in the Alberta oil and gas sector is the absence of a credible official estimate of total closure liability. The AER formerly produced a calculation of the total deemed liabilities every month as part of the Liability Management Rating (LMR) Results Report (the final LLR deemed liability was $36 billion in July 2024) but those estimates were calculated using average liability cost estimates set by Directive 011 that are known to be inaccurate (Directive 011 was recently updated but only in relation to decommissioning (that is, abandonment or plugging) costs, whereas remediation and reclamation costs appear to be the most underestimated). The AER official estimates hovered in the low to mid $30 billion dollar range since 2015, an estimate that always excluded any and all pipeline segments. The AER has acknowledged the errors in these estimates, and the Auditor General has described many of them, but the public continues to receive conflicting and inconsistent estimates of total closure liability (see Waiting for a Credible Cost Estimate of Oil and Gas Closure Liabilities and the Problem with CARL for more details on this posted by one of us in May 2024). In 2018, a leaked internal AER presentation blew the roof off of published AER estimates. That presentation suggested that conventional liabilities are probably closer to $100 billion, pipeline liabilities are around $30 billion (based primarily on estimates of federally regulated pipeline liability) and $130 billion for oil sands liabilities, bringing the total to an eye-watering $260 billion.

Closure liability policy in Alberta was significantly transformed in 2020 when the federal government provided Alberta $1 billion to distribute to oil and gas companies for closure work (although $137 million of that money was returned unspent). In exchange for that funding, the Alberta government announced a new policy direction for the regulation of conventional oil and gas closure liability in the form of the Liability Management Framework. The Liability Management Framework has four components: (1) reduce the number of inactive sites with closure work; (2) assess applicants and existing licensees to ensure their solvency and operational record demonstrates an ability to meet closure and other regulatory obligations; (3) expand the mandate of Alberta’s Orphan Well Association to enhance its ability to undertake closure work for sites without a solvent owner; and (4) develop a regulatory program to address closure liability associated with legacy and post-closure sites for which there is no responsible owner.

For the most part, the AER is responsible for implementing and administering the Liability Management Framework. The Responsible Energy Development Act, SA 2012, c R-17.3, gives the AER its overall mandate, authority, and power to regulate the development of oil and gas resources and closure work. More specific powers and legal obligations are set out in various other enactments. For example, with respect to pipelines these enactments include the Pipeline Act, RSA 2000, c P-15, and Pipeline Rules, Alta Reg 125/2023. These enactments also provide the AER with power to make rules with respect to liability management. Those rules are found primarily in two directives: AER Directive 067 – Eligibility Requirements for Acquiring and Holding Energy Licences and Approvals and AER Directive 088 – Licensee Life-Cycle Management. AER Manual 023 sets out and explains specific procedures used by the AER to assess liability risk of applicants and licensees, as well as implement minimum mandatory closure spending requirements on inactive sites.

The AER website is a labyrinth in terms of explaining how the regulator administers and implements liability management, with many pages conveying information in a manner that is duplicative, convoluted, and confusing (see e.g. here, here, here, here, here, and here). Perhaps the best place to start is the Liability Management page, which provides a very cursory description of the components of the 2020 Liability Management Framework. This page mentions that legislative amendments were required to implement the Liability Management Framework, including amendments to AER Directive 067 and the enactment of Directive 088, and provides links to other pages that give some explanation to specific aspects of liability management: holistic assessment and licensee capability assessment, licensee management program, inventory reduction program, and the license transfer process. All of these pages are also linked to the Liability Management Programs and Processes page, along with additional pages such as the Orphan Well Association, liability management rating and reporting, mine financial security program, and insolvency. The AER website provides very little information on security deposits and legacy and post-closure sites, located on the general Liability Management page.

Collectively, the purported purpose of these requirements is to reduce unfunded closure liability in Alberta. To accomplish this, the requirements mandate an annual amount of spending by industry on closure work. They also provide the AER with the power to holistically scrutinize the financial and operational capacity of applicants for new licenses and existing licensees to perform closure work, and to control those risks by refusing to grant or transfer licenses or imposing conditions such as security deposits. The AER describes the licensee capacity assessment as the ‘backbone’ of the holistic approach:

The licensee capability assessment (LCA) is the backbone of our holistic assessment of companies throughout the energy development life cycle in the oil and gas sector. Introduced through Directive 088: Licensee Life-Cycle Management, the LCA considers a variety of factors to help us evaluate a company, including their financial and liability risk, their performance compared with similar companies, and other operations, closure, and administrative factors, with compliance history being considered throughout.

The information that feeds into the LCA comes from several sources, including financial information that companies are required to provide us through Directive 067.

(AER, “Holistic assessment and Licensee Capability Assessment”)

The AER has been gradually developing and implementing the Liability Management Framework since 2020, but there are still large gaps in the framework. The AER continues to make incremental changes that do not address the substantive causes of the unfunded liability problem or reduce liability.

As it has developed, the key parts of the framework are the holistic assessment and licensee capability assessment, the closure spend quotas (which are set without sufficient planning to be effective), the closure nomination program, and an expanded role for the Orphan Well Association. Major parts of the framework are still missing, and key elements remain severely underdeveloped. The AER has not developed any approach for legacy and post-closure sites. The AER has not developed the ‘licensee special action’ component described in the 2020 government policy announcement.

Perhaps the most significant undeveloped component of the framework is that the AER has still not established an overall regulatory approach for collecting security. The collection of security for closure (both the decision on whether to require a security deposit and what the amount of that security is) continues to be entirely at the discretion of the AER (which, as repeatedly demonstrated, is captured by industry). It remains impossible for the public to know exactly when and under what circumstances the AER requires security deposits from industry to meet closure liabilities and whether those security amounts are enough to ensure regulatory framework avoids socializing the losses to the public.

When companies apply for new licenses, or to transfer existing licenses, the AER also collects information on unpaid municipal taxes. This requirement was initially imposed on the AER in 2023 by the Minister of Energy in Ministerial Order 043/2023, wherein the Minister also directed the AER to require companies to reduce taxes payable below the threshold amount of $20,000 or give evidence of repayment arrangements with the municipality. Questions have arisen on the extent to which the AER follows this Ministerial direction. In December 2025, the Narwhal published an investigation (see here) that revealed in September 2024 the AER approved the transfer of licenses to a transferee that owed more than $200,000 in unpaid municipal taxes. In addition, exceptions to the unpaid taxes requirement were added following Ministerial direction in October 2024 (discussed in detail here). Most significant here is that the AER may approve transfers of oil and gas licenses out of the inventories of bankrupt companies so long as the transferee owes less than $20,000 in municipal taxes. Accordingly, unpaid municipal taxes are not a roadblock to the strategy of new oil and gas corporations being created specifically to absorb particular assets from bankrupt oil and gas corporations (as occurred with Manitok).

We remind readers that the AER’s performance on implementing the Liability Management Framework was the subject of a report by the Alberta Auditor General in March 2023. ABlawg commented on this report here and here. One key finding of this report is an absence of meaningful transparency from the AER. This problem manifested in two ways: (1) a lack of external performance measures on closure work; and (2) failure to report meaningful information to people in Alberta. The absence of transparency makes it difficult for the public to assess the AER’s performance and to hold the AER accountable for its regulatory functions in this area. The amount of effort put by the Narwhal into the 2025 investigation on unpaid municipal taxes (discussed above) is a revealing illustration of how elusive transparency is at the AER.

Specific deficiencies noted by the Auditor General in how the AER reports its performance to Albertans include the following:

Specific goals to ensure accountability for results as it changes key parts of its liability management system have not been established. For example, what AER views as a reasonable and sustainable level of inactive closure liabilities given level of industry activity, economic factors, and other considerations? What is the current closure liability amount and what is an acceptable level? What does AER define as timely restoration of inactive sites and what is the goal for timeliness?

The Ministry of Energy and AER annual reports contain data about the amount of closure activity and spending in Alberta. However, they do not report on the total number of inactive sites in Alberta making it difficult for Albertans to assess if net progress is being made to reduce inactive sites.

AER lacks external performance measures to demonstrate whether its liability management programs are working. The lack of public reporting on performance measures with targets also makes it difficult for Albertans to know if risks are being adequately managed and that the cleanup being done is sufficient. Reporting on activity alone is not enough to effectively measure the performance and achievement, or lack thereof, of goals.

AER’s most recent estimates, at the time of writing, for industry-wide (active and inactive) closure liabilities in Alberta ranges from $30 billion for wells and facilities to $60 billion if pipelines and more recent information are included. …. AER also has not defined what it considers to be an acceptable and sustainable level of closure liability.

An overall liability estimate includes both active and inactive sites, where active sites may not need closure work completed for years. Contrasted with inactive sites that may require closure work sooner. Also, the potential financial risk to the public depends on who is responsible for the liabilities.

(“Liability Management of (Non-Oil Sands) Oil and Gas, Report of the Auditor General March 2023” at 22 – 23)(emphasis added)

As a final piece to this overview, we note that the Alberta government has commenced with potentially significant changes to the liability management framework, following recommendations made in the April 2025 Mature Asset Strategy – the product of a closed-to-the-public selection of stakeholder working group deliberations. In September 2025 we critically examined the Strategy and concluded it is largely a smoke and mirrors exercise on Alberta’s unfunded closure liabilities problem, offering almost nothing substantive to address fundamental deficiencies in the liability management framework: (1) a lack of transparency that impairs accountability and public scrutiny for closure liability decisions; (2) too much reliance on discretionary power to implement legal requirements that would mitigate and address closure liability (e.g. security requirements); and (3) too much industry influence in the design of a liability management regulatory framework. An implementation of the Strategy threatens to further entrench industry influence and socialize closure liabilities to taxpayers, as Bob Weber explained in “Dirty Cleanup Scheme: The latest plan to dump industry’s mess onto taxpayers”.

The 2024 Report on Liability Management

The 2024 Report still does not provide the information called for by the Auditor General and fails to set out goals or targets to assess the effectiveness of AER policy design or implementation. As with the 2022 and 2023 reports, in too many places the 2024 Report reads more like industry promotional material than a credible regulatory performance report.

Sections one and two of the 2024 Report follow nearly identical formatting to the 2023 report, but the AER changed the format of the remainder of the report. This inconsistency adversely impacts a comparative analysis – something that should be readily achievable in annual performance reports. This is why, for example, securities regulators insist on a standard and highly regimented format in the annual and ongoing public disclosure by reporting issuers.

The 2024 Report does not include a dedicated section on the Orphan Fund Levy (this was section three in the 2023 Report). Instead, the 2024 Report has mixed a small bit of OWA activity together with data on closure spending by industry. The 2023 report had a two-page section with four figures on the orphan program and the activities of the Orphan Well Association (OWA). Notably, the size of the OWA closure inventory by year and the OWA’s estimate of remaining closure costs are not included in the 2024 Report (this information was in the 2023 Report at 10-11). This information is available in the OWA’s Annual report (which one of us summarized here), but the removal in the 2024 Report is suspicious and the skeptical reader would speculate this information was not included because the news is bad: the OWA’s inventory is now at a record high, and the OWA’s estimate of remaining closure costs hit a record $1.12 billion. Figure 10 (at 13) does show the OWA’s total closure spend fell again from $180 million in 2022, to $144 million in 2023, to $119 million in 2024. The decrease was expected given the OWA’s obligations to pay back government loans. The orphan program has more closure work than ever and a declining yearly budget to address that work. The orphan program is obviously underfunded and the absence of this information in the liability management performance report is a glaring deficiency.

Section One: Conventional Oil and Gas Infrastructure

Section one provides data on the production status of wells, facilities, and pipelines. A new bar graph is added as figure 3 in the 2024 Report showing decommissioned wells by age (at 4). Figure 3 shows two interesting things: (1) from 2000 to 2014, between 25% and 50% of wells decommissioned each year were less than a year old, suggesting industry was drilling and decommissioning significant numbers of dry wells each year, and (2) beginning in 2016 and accelerating since 2021, industry has been decommissioning more wells drilled more than 20 years ago.

The skeptical reader wonders if the AER added this graph (alongside the bar graph showing decommissioned wells by years inactive (at 4)) simply to highlight its statement that in 2024 industry decommissioned more older wells and direct attention away from the more troublesome trend that the bar graphs in this section illustrate: the annual number of wells decommissioned has been falling since 2021. Almost 12,000 wells were decommissioned in 2021 and less than 6,000 wells were decommissioned in 2024. The text in section one makes no mention of this downtrend in decommissioned wells.

Figure 4 shows how long wells were inactive prior to decommissioning. The data in figure 4 changed from 2023 to 2024 because the AER stopped including wells that were decommissioned before becoming officially ‘inactive’ (generally meaning they were decommissioned less than a year after final production). The 2023 report said that “Approximately 36 000 wells inactive for ten or more years remain.” (2023 report, page 4), this sentence was deleted from the 2024 report instead of being updated, but table 4 shows slightly more than 2,000 wells inactive for ten or more years were decommissioned in 2024, so Alberta had approximately 34,000 wells inactive for ten or more years at the end of 2024.

Section Two: Estimated Liability and Licensee Capability

Section two reports on estimated liability. As noted in our discussion of the 2022 and 2023 reports, we continue to emphasize this is not a reliable estimate as the AER persistently uses inaccurate figures for estimating well reclamation costs – but the official estimate in the 2024 report is $36.6 billion consisting of $23.4 billion for inactive sites and $13.2 for active sites.

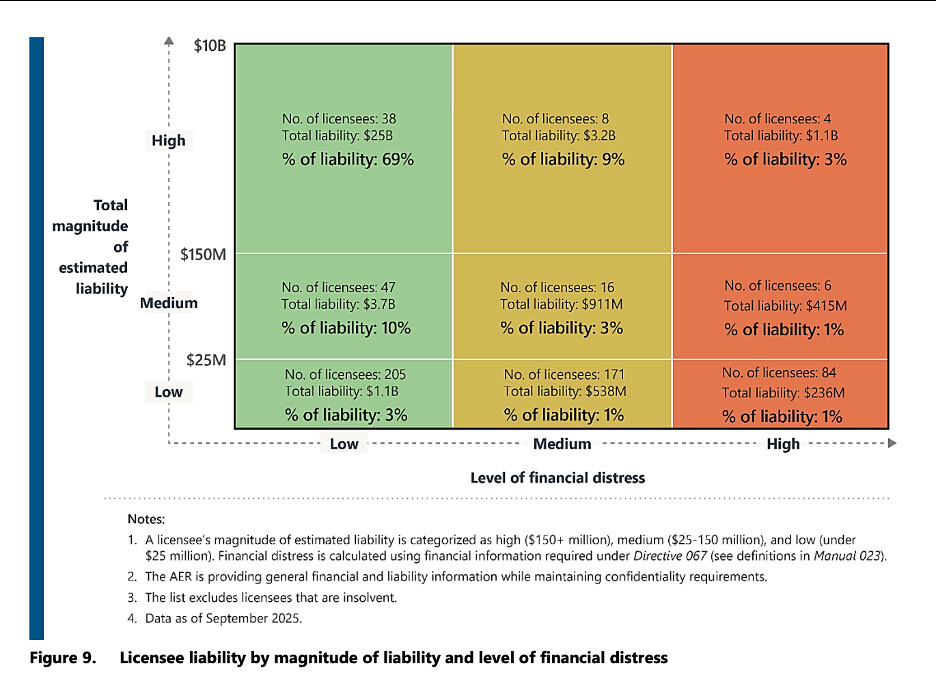

The 2024 Report provides an updated risk matrix table in figure 9 (at 9) on closure liability in the same format as presented in the 2022 and 2023 reports:

The table in figure 9 still has limited utility, since some numbers are rounded to the nearest billion dollars, other numbers are rounded to the nearest hundred million dollars, and all the numbers are calculated on the basis of underestimated reclamation liabilities.

The 2024 Report shows reductions in liability in the “high financial distress” column from the 2023 numbers, but this is misleading because the numbers do not reflect insolvencies (see the discussion of some recent major oil and gas insolvencies here.). In our view, the companies in the “high financial distress” category are bound for bankruptcy proceedings and most of the closure liabilities will end up with the OWA, which receives only a fraction of the funds needed in annual levies from industry to pay for their closure within a reasonable time.

The 2024 Report provides no information whatsoever on how the AER has used or considered this information in its licensee capacity assessments or company-specific closure work quota requirements. We made the same observations with the 2023 and 2022 reports, and curiously the 2024 Report offers no comparison with data in the previous report.

The 2024 Report provides better data on license transfers compared to the 2023 Report (at 10). The data now shows year-to-year comparisons on transfers and security collection for 2022, 2023, and 2024. The data shows at least two major problems. First, the AER has failed to collect meaningful security when licenses are transferred to a licensee with less financial capability. Relative to the inactive liability transferred, the AER collected 7% in 2022, 2% in 2023, and 1% in 2024 (Table 1, at 10). These are the worst form of transfers, as the transfer from a more financially capable licensee to a less financially capable licensee leaves the public (and the OWA) at higher risk, this is the “liability dumping” problem. The report offers no explanation on why the AER collected only 1% of the estimated inactive liability. Second, all security collected as a percentage of liability is too low because it is calculated on the basis of (grossly) underestimated reclamation liability (one of us described the problem in detail in a May 2024 post), and because the AER is collecting security only relative to inactive liability and ignoring the liability of marginal assets, which the AER is aware do not produce enough to pay for their own closure.

In contrast to the collapse in security collection for transfers to less financially capable licensees, the AER has gradually been collecting more security when licenses are transferred to new licensees (9% in 2022, 18% in 2023, and 21% in 2024). Those percentages are still absurdly low, but the movement is in the correct direction. This positive trend makes the AER’s tiny security collection for transfers to less financially capable licensees even more baffling.

Section Three: Closure Spend and Activity

Section three purports to provide some information on how the closure quotas are set: “Commodity prices are a significant factor in determining the annual industry-wide closure requirements.” (at 11) The report notes that in 2024, oil prices were high compared to historical averages, and natural gas prices were low compared to historical averages. But this does not provide any real explanation for the amounts of the closure quotas, since the relationship between commodity prices and the closure quotas is not explained, and there is no obvious method for how the amount of closure work should be connected to high or low commodity prices. Is the AER basing the closure quota on industry ability to pay, or on level of risk to the public? Those approaches would give opposite answers for the relationship between commodity prices and closure quotas.

This section includes a paragraph on the closure nomination program. Two of us recently commented on the design and implementation of this program in A Review of Closure Nomination for Inactive Oil and Gas Sites and AER Updates to Directive 088. The upshot of our assessment is that the effectiveness of the closure nomination program is uncertain thus far because of poor transparency and excessive AER discretion in determining whether a nominated well is eligible for mandated closure work. We did, however, provide some analysis of data which is more than can be said for the two sentences provided by the AER in the 2024 Report: “In 2023, 62 sites were nominated under the closure nomination program, with a $374 000 spend reported. In 2024, 48 sites were nominated for closure under the closure nomination program, with a $1.46 million spend reported.” (at 11)

Industry spent $900 million on closure work, which exceeded the $700 million quota set by the AER. While the AER attempts to spin this into a positive outcome, it is important to remember three things: (1) the closure quota set by the AER is a meaningless benchmark because it is set without any transparent correlation to addressing the total closure liabilities; and (2) the trendline on closure work strongly suggests this amount of closure spend is merely holding the line and maybe preventing the closure liability problem from getting worse in the conventional sector; and (3) a report on industry-wide spend fails to provide useful information such as which parts of industry are exceeding their closure quotas and why are they doing so. Perhaps some financially strong licensees are exceeding their closure spend to attempt to reduce their total liabilities and therefore their share of the annual orphan levy, or maybe cost overruns on closure projects are driving the closure spend up higher than what industry is planning on at the beginning of the year. The reader is left to wonder. The 2024 Report does not contain an explanation.

Figure 12 (at 14) also shows that the closure spend has remained concentrated on decommissioning (57% of the closure spend) rather than the remediation or reclamation work needed to obtain a reclamation certificate. This trend is likely connected to the AER’s underestimate of reclamation liability costs. Licensees obtain larger reductions in their estimated liability for decommissioning spending than for reclamation spending. The AER needs to fix their reclamation liability estimates to correct this distortionary effect.

The annual comparative data on decommissioning and reclamation work by industry shows that overall numbers of sites decommissioned or certified as reclaimed has fallen successively in each of 2022, 2023, and 2024 (at 15 – 16). The Report provides no discussion of this troublesome trend, a glaring omission in a “performance report”.

Section Four: Impact on Liability Estimates

It is unclear to us why the AER separated this section from section three (unlike previous years when the two were combined), other than maybe to keep four sections in the Report and make up for the striking absence of the orphan well levy section? Odd.

Noteworthy information here includes the fact that the number of companies who fail to comply with the mandatory spend requirement rose from 54 to 69, representing a drop from a 91% compliance rate to an 85% rate (however the 2024 Report does not actually provide this comparative data – you have to read the 2023 Report (at 17) and compare that with the 2024 Report (at 18)). As well, 22 licensees failed to meet their closure quotas for 2022, 2023, and 2024 (see the list on page 19). The AER does not appear to have much of a strategy for dealing with these licensees.

Conclusion

Unlike in 2023 and 2022, the AER did not issue a news release about the 2024 Liability Management Report, but that may relate to AER staffing or resourcing. The AER has not issued any “news releases” since August 2025, and there are reports that the AER “laid off the majority of its communications staff — including media relations”.

In terms of data disclosure, the 2024 Report is similar to the 2023 report except for the omission of data on the orphan program. Once again, the report is hardly an assessment of “performance”. The report still does not contain any target levels or planned timelines for bringing unsecured active, marginal, and inactive closure liability down. This information is necessary to know what the current situation is, what the AER’s strategy is, and to assess whether the AER’s strategy is working. Without knowing what the goals of the liability management framework are, it is not possible to determine whether it is succeeding or failing, or if the framework has been rationally designed.

The 2024 Report fails to provide any meaningful analysis of comparative data across years. It also seems like the report selectively highlights information to give a positive spin on industry closure work, and chooses not to discuss information that would reflect poorly on industry or the AER itself.

In terms of the operation of the liability management system, the 2024 Report shows problems (or, in the case of the orphan program, omits evidence of problems). The orphan inventory is larger than ever, and the (official) estimated total conventional closure liability is higher than ever. Closure spending peaked in 2022, fell in 2023, and fell again in 2024 (although it did not fall as much as we expected (because of industry overspending the closure quota). Reversing the trend would require higher orphan fund levies and higher mandatory spend quotas, which the AER has been reluctant to impose. The changes made to the liability management system since 2020 have only slowed down how quickly closure liabilities are accumulating. The closure problem is not fixed or being fixed.

In 2023, we published a critical evaluation of the closure liability policy in “A Made-in-Alberta Failure: Unfunded Oil and Gas Closure Liability”. Our analysis was informed by a historical review of Alberta’s approach to managing closure liabilities over the past 40 years in order to assess whether the Liability Management Framework is properly designed to achieve its objective of getting closure work done and ensuring the polluter — not Alberta taxpayers — pays for it. The conclusion of the study is that three factors that have contributed to Alberta’s historical failure to effectively manage closure liabilities remain problematic today in the design of the Liability Management Framework and its current legal and policy framework: poor transparency, excessive discretionary power exercised by the AER on a case-by-case basis in place of fixed rules, and a regulator captured by industry interests. We maintain that these factors remain problematic with the AER and how it is administering the Liability Management Framework.

Last year, we identified what we view as the three most pressing closure liability management issues the AER needed to address in 2025. The AER has not taken action on any of these issues and so our recommendations remain the same:

(1) The extremely long running lack of transparency about the cost of oil and gas closure liabilities: The AER’s official liability estimate is too low, the AER knows it, and a sound liability management framework cannot be built on an inaccurate liability estimate. Well reclamation cost estimates must be updated and pipeline closure costs must be added to the total estimate. The AER must provide the public a closure liability estimate based on the best available evidence.

(2) The lack of transparency on setting the mandatory closure spend and orphan fund levy: The AER must publicly set goals and timelines for addressing the closure liability problem so that the auditor general, the public, and the AER itself can assess whether the new framework is working as intended. The AER also continues to set the Orphan Well Levy in consultation with industry and out of public view.

(3) The excessively discretionary approach to financial security collection: The AER needs to select a fixed approach that collects more security during transfers and as assets age that aligns with publicly stated goals for closure liability management. The discretionary approach to financial security collection is problematic for a number of reasons, including that it leads to bizarre outcomes like the drop in security collection for transfers to less financially capable licensees that occurred in 2024.

The 2024 Report is a step backwards from the 2023 Report. The decision to omit a dedicated section on the orphan well association closure activity is unexplained. The report reads even more like industry spin on closure work than in previous years. While more data is provided in 2024, there is almost no discussion or analysis of that data (particularly the data that would show existing or brewing problems with the liability management framework). As the Auditor General wrote in 2023: Reporting on activity alone is not a performance assessment. The inconsistencies in how data is reported between 2023 and 2024 significantly impairs a comparative assessment, which is very problematic for a “performance” report.

Lastly, the (unwarranted) positive spin on industry closure activity and AER performance on liability management contained in this 2024 Report leads us to wonder how this correlates with the 2025 Mature Asset Strategy which (correctly – although without proper justification) asserts that there are significant problems with the implementation of the liability management framework. Which is it: is the liability management system effective and stable or is the liability management system so ineffective that it needs to be replaced?

For all these reasons, we grade the 2024 AER Liability Management Performance Report as follows:

F

This post may be cited as: Drew Yewchuk and Shaun Fluker, “Grading the 2024 AER Liability Management Performance Report” (5 February 2025), online: ABlawg, http://ablawg.ca/wp-content/uploads/2026/02/ Blog_DY&SF_AER2024.pdf

To subscribe to ABlawg by email or RSS feed, please go to http://ablawg.ca

Follow us on Twitter @ABlawg